I like to study successful investors, as part of my effort to continuously improve on my process. Tom Russo is one such investor. I believe I can learn from him.

Between 1990 and 2021, his fund, Semper Vic Partners delivered a total return of 12% to its investors. This was better than the 11.10% return of Dow Jones Industrials average and 10.50% return on S&P 500. Russo invests in a few select industries like industry food, tobacco, media and beverages in which companies have historically proven their ability to generate high and sustainable returns on capital.

His strategy seems to focus on the type of solid blue chip companies that deliver slow but steady performance. These businesses tend to generate a ton of free cashflows and tend to distribute a ton of cashflows to shareholders in the forms of dividends and buybacks, while still growing over time. In addition, these businesses have a product or service that is relatively recession resistant. Such businesses tend to think about the long-term, but sadly are rarely available at discounted valuations. Russo says investors should look to buy businesses with some margin of safety that comes when these businesses are available at a sufficient discount from their actual value.

The businesses he focuses on are companies with leading brands, such as Nestle or Brown Forman, which operate globally. They have powerful brands that are globally known, which give them the ability to enter new markets and grow market shares in different countries. A strong brand commands price elasticity and drives recurring revenue and high return on capital, and reduces the risk of the business model. Price elastic demand is crucial because loyal consumers will be willing pay a higher price should inflation drive up ingredient cost and the company needs to maintain its margin through higher prices.

This has been the case in emerging markets over the past 30 years. Riding the wave of increased prosperity and emerging growth has been beneficial for global brands. When they enter, the market may not be developed, which means that these brands should have the capacity to suffer throughout the initial phase of market development and the development of the country they just launched operations in. However, as the country grows its economy, its consumers grow their disposable income, the market demand increases, which is good for business. These businesses also have the capacity to reinvest a portion of their income, at a high hurdle rate of return, in order to build the base for future dividend growth. He basically looks for companies with two characteristics – the capacity to suffer and the capacity to reinvest.

He was able to invest in companies like Nestle as early as the late 1980s and early 1990s, when it was much harder for US investors to access this security. He does use Nestle as an example of a company that can enter a new market and invest there to build up its operations with a long term focus. It can "suffer" low profits initially, but with the expectation to make more profit down the road. This of course is possible because of the diversified nature of its global operations, which can temporarily subsidize future ventures. Nestle shareholders of course have enjoyed a streak of rising dividends since 1995.

Tom Russo also looks at family controlled businesses, because he has found that these types of companies tend to think long-term, and avoid the short-term pressures of Wall Street. These are businesses that do not care about beating a quarterly estimate by Wall Street. Instead, they think about years, if not decades, down the road. This is particularly powerful when you are dealing with some of the staples, which have more predictable demand for their goods. These companies are willing to reinvest for the future, even if it means some short-term pain.

The nature of the companies he invests in shows me that he invests in consumer products companies like food, beverage, tobacco and media. A lot of these businesses have been around for a long time, have strong brands, some pricing power and a relatively inelastic demand. They are market leaders in their niche, and would likely be around decades from now. An investor who buys at the right price would likely generate a steady stream of growing dividends, fueled by a steady compounding in earnings per share over decades. These are the types of companies with a long future runway that patient buy and hold investors like to invest in.

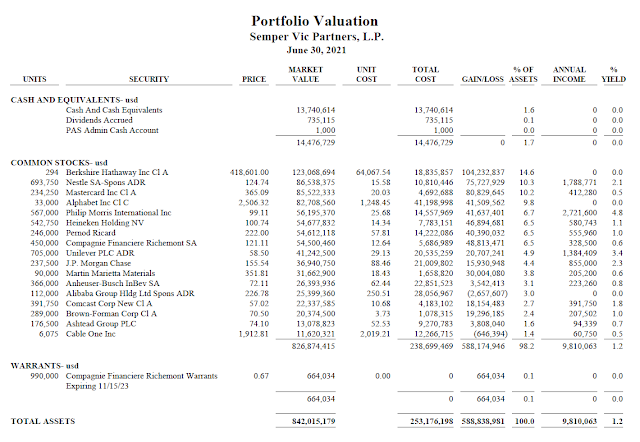

If you look at the companies in his portfolio, you can see that these companies have strong global brands, they have benefitted from international expansion, and the rise in international consumerism. These companies include Nestle, Mastercard, Unilever, Philip Morris, Brown-Forman, Google.

You can read more about Tom Russo here.

There is a talk he did on Global Value Investing.

He also explained his strategy with Consuelo Mack a few years ago here.

I enjoyed this article from Morningstar: Tom Russo: Good investors must have the "capacity to suffer"