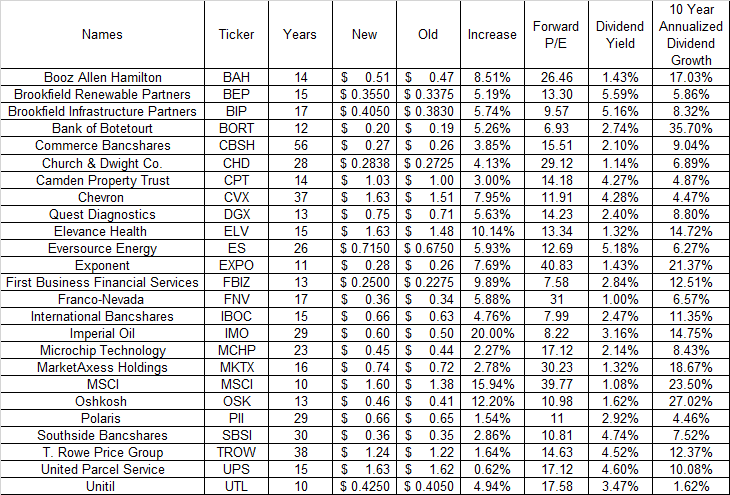

My retirement strategy is focused on living off dividends. Dividends are more stable, predictable and reliable than capital gains. Dividends also tend to increase faster than inflation over time. This is what makes them a better source of retirement income than relying on selling stock to pay for expenses.

This makes sense, because dividends come from cashflows, which tend to be more stable. Asset Prices on the other hand tend to oscillate between being undervalued and a period of being overvalued. Asset prices in the short run are driven by fear, greed, expectations.

If you happen to retire when prices are undervalued, you'd be selling low, and increasing your chances of outliving your money. I do not want to run out of money in retirement. Hence, I do not plan on selling assets to fund expenses in retirement. I plan to use income generated from investments to pay for expenses in retirement.

I also to think about the topic of Generational Wealth quite a bit as well. I wrote a little bit about the concept of Generational Wealth before. I think about it through the lens of Dividend Growth Investing.

Typically my thought process goes something like this:

If my great-grandparents had invested in equities 100 years ago, everyone in my family would be a multi-millionaire today. We would all be set for life.

But sadly, they didn't.

So, I have to be that great-grandparent now...

As you can see, I often ponder about generational wealth.

There are many obstacles to accumulating it, such as:

- Poor investment returns

- Lack of savings

- Impatience

There are many obstacles to keeping it too such as:

- Poor investment returns

- Taxes

- Overspending

- Fees

- Confiscation

A big obstacle to Generational Wealth is heirs who squander the funds. Families that build and maintain generational wealth take to instill a basic set of values, which are passed down on future generations. Transmitting values through generations is how families manage to maintain wealth, despite anything that happens.

The most important principles in my opinion center around:

1. Working hard

2. Living within your means

3. Power of compounding

4. Intelligent investing

5. Giving back

Building wealth is one important skill to have. It requires living within your means, and spending less than what you earn. Then you need to invest the difference intelligently.

Maintaining wealth is another important skill to have. It means spending less than what your investments generate, in order to avoid running out of money. We all have to assume that the money is invested intelligently.

It's fascinating to think about Generational Wealth with two families that built their fortunes around the same time in the 19th century. The Rockefellers and The Vanderbilts.

The Rockefeller family has been able to successfully remain wealthy, and provide for hundreds if not thousands of offspring, through several generations. The person who built the fortune was J.D. Rockefeller, who founded Standard Oil - an energy conglomerate.

The Vanderbilt family has not been able to successfully remain wealthy. The person who built the fortune was Cornelius Vanderbilt, who owned railroads. Around 80 years after the death of Cornelius Vanderbilt, there was not one single family member that was even a millionaire.

Both families spent lavishly. But only the Rockefeller family is wealthy.

I think that lavish spending is just one of the reasons behind running out of money.

The second reason, which is very important actually, centers around investment returns.

My working theory is Vanderbilt's fortune was concentrated in transportation, which didn't do well first half of 20th century and had massive dividend cuts in 1930s

When you spend a lot and income dries up you start eating principal..That's how you run out of money.

Standard Oil did better- but trusts helped too.

This is Exxon Mobil stock performance ( I don't have data for other Standard Oil companies, and other investments)

Their dividends didn't suffer too much in the Great Depression either. See Exxon's dividend history 1911 - 2014.

Ultimately, the Vanderbilts seem to have had most of their money in the transportation sector, like railroads. Their investments had a hard time generating consistent returns during the first half of the 20th century. That Great Depression must have severely cut dividend income, and to maintain standard of living, descendants had to resort to selling stock at low prices. This meant that they could not participate in the eventual recovery in those stock prices later on and subsequent growth in dividends. That because they sold their shares at low prices, in order to maintain a high standard of living.

I am sure there are other reasons as well, but it definitely strikes me as important that you want to have investments that make money when you try to live off them. If they do not generate good returns, that retirement will not be successful.

The Rockefellers seem to have had most of their money in the Energy sector, like Oil and Gas and Pipelines. This sector seems to have been doing well in the first half of the century, and the last half as well. It seems like it was not as affected by the Great Depression as transports. Dividends largely remained, and weren't cut as drastically as in the transportation sector. Despite their lavish spending, they didn't run out of money, because their investments did well even during the depression.

These are fascinating observations, in light of my obsession with retirement planning and making sure one doesn't run out of money in retirement. I believe the following lessons can be applicable to rest of us as well, even if we do not deal with billions of dollars (at least I am not, yet)

Ultimately, there is a bit of a dose of luck as well as survivorship bias. We could have two families with a similar set of spending. But if the first family picks poor investments it increases its risk of running out of money. If the second family picks good investments, they are less likely to run out of money.

Focusing on things within your control is definitely a part of a winning strategy. One needs to continue having a certain dose of frugality, and avoid excess, as a way to counteract whatever life will throw at them. This also includes selecting the investments one owns, the holding period, managing the costs and ensuring proper diversification.

The lesson is to diversify investments, and be prepared to reduce spending if investment returns turn out to be less than expected. One needs to live within their means in the accumulation phase, in order to accumulate their nest egg. They also need to continue living within their means in retirement as well.

Spending principal is a good way to increase your chances of running out of money in retirement, particularly when share prices are low. Living off dividends in retirement is a more robust way to generate retirement income, which reduces the probability that one runs out of money in retirement. If you focus on the dividend income generated by that portfolio, you know how much you can spend. This removes a lot of the guesswork. It also provides an almost real-time assessment of current conditions that allow the retiree to correct and adjust course. It also provides the retiree with an early warning if things do not go as planned.

It's also important to spend time educating the next generation, in order to reduce the risk of them blowing the nest eggs. Families that successfully manage to maintain generational wealth tend to transmit a set of values across generations. Those values include the importance of hard work, frugality and entrepreneurship. However, they also build controls in place, such as strategic use of trust funds and financial professionals/a family office, to oversee management of financial affairs for the family members. Having restrictions on how much can be withdrawn annually from the nest egg, and also having some professional management could be helpful to future generations, even if it does come at a cost. Navigating the ever increasing complexity of tax and estate laws can be challenging however, which is why a family office could help in this endeavor.

Encouraging family members to also build out their own human capital on top of investments that they own is very important as well. That can help them focus on making a difference in the world, and monetize specific talents that they have, while also serving a purpose in life. Work provides purpose in life to many, and helps keep them grounded.