Diageo plc (DEO) produces, distills, brews, bottles, packages, and distributes spirits, beer, wine, and ready to drink beverages. This international dividend company has increased dividends for 25 years in a row. The company’s peer group includes Brown-Forman (BF.B), Suntory, and Constellation Brands (STZ).

The company’s latest dividend increase was announced in January 2023 when the Board of Directors approved an 5% increase in the interim dividend to 30.83 pence /share. The final dividend had been increased by 5% to 46.82 pence/share in October 2022.

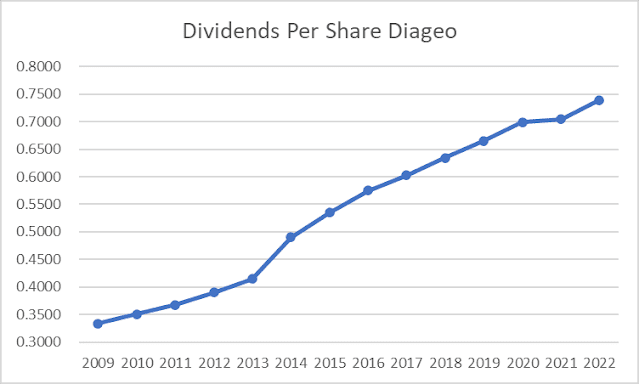

The annual dividend payment has increased by 6.30% per year since 2009, which is in line with the growth in EPS.

A 6% growth in distributions translates into the dividend payment doubling every twelve years on average. Between 1998 and 2008 dividends per share doubled. The next double took about eleven years to achieve, which is not bad.

Dividends on the ordinary shares are normally paid twice a year: an interim dividend in April and a final dividend in October. The approximate split between the two payments is 40:60.

Diageo trades on NYSE as American Depository Receipts. Each receipt is equivalent to 4 shares traded in London. As such, there is a small fee by the custodian bank that issues the ADR’s in the US. Being a British Company, there are no dividend withholdings at the source. You still owe tax to Uncle Sam in a taxable account however.

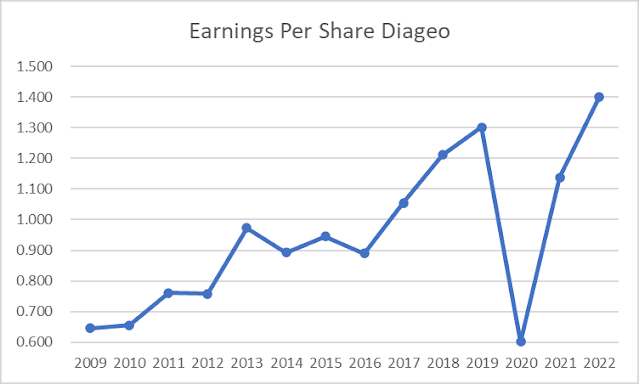

The company has managed to deliver an 6.10% average increase in annual EPS in British Pounds since 2009. Diageo is expected to earn 164 pence per share in 2023In comparison, the company earned the equivalent of 140 pence/share in 2022. Each American Depository Receipt (ADR) that you can purchase on the NYSE is equivalent to four shares that are traded on the London Stock Exchange.

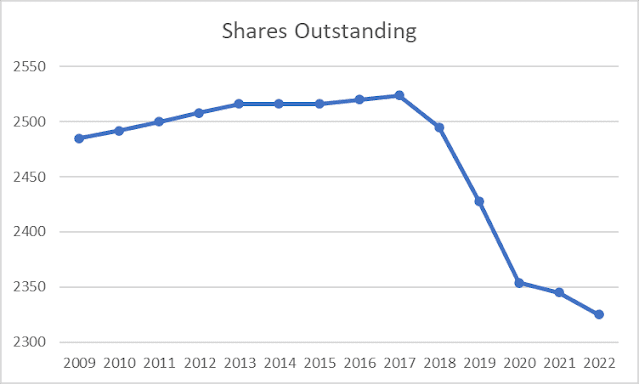

Between 2009 and 2022, the number of shares decreased from 2.485 billion to 2.325 billion.

Diageo owns a portfolio of strong brands, with wide consumer appeal, which are usually number one or two in their respective categories. A few include Smirnoff, Johnnie Walker, Guinness, Baileys, and Captain Morgan. The company also has a wide distribution network on a global scale, which might be difficult for a competitor to replicate. Diageo is the largest spirits company in the world, which provides it with the advantage of scale, relative to its competitors.

Future growth could be driven by organic growth of its premium brands as well as through strategic acquisitions. The company has also focused on its core competencies, by disposing of Pillsbury and Burger King in the early 2000s. North America accounts for one third of sales but over 45% of operating profits. Emerging markets in Asia, Africa and Latin America account for 43% of sales by 29% of operating profits. Europe accounts for 24% of sales and 25% of operating profits. Continued investments in strategic emerging markets could translate into higher sales in the future, particularly as the number of middle class consumers who will be able to afford premium drinks rises significantly.

The company has really high return on equity, which is common for most high quality dividend payers that do not require a lot of equity to operate the business. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

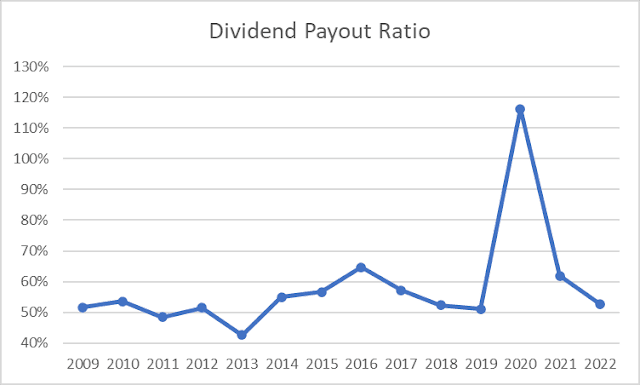

The dividend payout ratio has remained around 50% for most of the time (excepting during the Covid turmoil of 2020). A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.