The Procter & Gamble Company (PG) provides branded consumer packaged goods worldwide. It operates through five segments: Beauty; Grooming; Health Care; Fabric & Home Care; and Baby, Feminine & Family Care. Procter & Gamble is a member of the elite dividend kings list, which includes companies that have managed to raise annual dividends for at least 50 years in a row. That's not a small feat.

The company increased quarterly dividends by 3% to $0.9407/share yesterday. This dividend increase marked the 67th consecutive year that P&G has increased its dividend and the 133rd consecutive year that P&G has paid a dividend since its incorporation in 1890. (Source)

Management states that this dividend increase reinforces their commitment to return cash to shareholders, many of whom rely on the steady, reliable income earned with their investment in P&G.

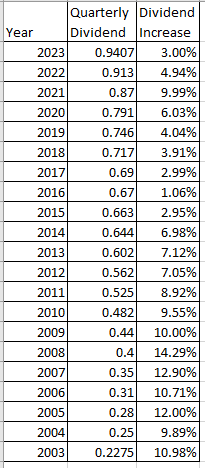

This dividend increase was at the slowest annual rate since 2017. It was also lower than my expectations. The table below shows the year that the company raised dividends, the new increased quarterly dividend payment for that year, and the rate of dividend increase for the year. It focuses on the past 20 years of dividend increases for Procter & Gamble:

The number of shares outstanding has been decreasing gradually over the past decade too.

At the current price, the stock seems overvalued at 25.71 times forward earnings. The stock yields 2.47%. Given the slow dividend growth, it does not seem like a good value today. Perhaps, it could be a better value on dips below $120/share.