Air Products and Chemicals, Inc. (APD) provides atmospheric gases, process and specialty gases, performance materials, equipment, and services worldwide. This dividend aristocrat has paid distributions since 1954 and increased dividends on its common stock for 40 years in a row.

The company's last dividend increase was in February 2022 when the Board of Directors approved an 8.50% increase to 77 cents/share. The company's largest competitors include Linde (LIN) and Air Liquide (AIQUY).

Over the past decade this dividend growth stock has delivered an annualized total return of 13.50% to its shareholders.

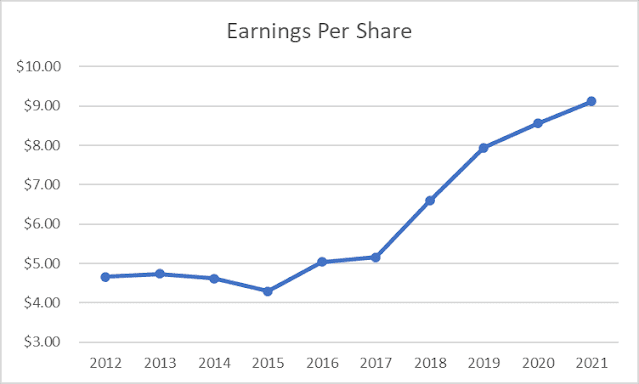

The company has managed grow earnings from $4.66/share in 2012 to $9.12/share in 2021. Analysts expect Air Products and Chemicals to earn $10.29 per share in 2022 and $11.62 per share in 2023.

Air Products and Chemicals is expected to post growth in sales, due to strong demand for industrial gases in rapidly growing economies in Asia. Long term growth will be driven by acquisitions, expansion into rapidly growing markets in South America and Asia. Recent acquisitions and projects in Saudi Arabia could drive future earnings growth.

Air Products and Chemicals streamlines operations and tries to manage costs strategically. In the past, the company has been shedding unprofitable operations, and focusing on cost cutting initiatives, in order to boost the bottom line.

In order to grow, the company should focus on increasing volumes in the merchant segment, plus executing new projects on time and budged in the tonnage segment, while focusing on plan efficiency improvements. In addition, focusing on major customers in the electronics and performance materials segment, while also introducing new offerings that could increase margins and returns. Other important opportunities include focusing on the pricing and the right mix of productivity and cost reductions, in order to hit profitability and margin goals set for itself.

The company operates under long-term customer supply contracts, particularly in the gases on-site business. These contracts principally have initial contract terms of 15 to 20 years. There are also long-term customer supply contracts associated with the tonnage gases business within the Electronics and Performance Materials segment. These contracts principally have initial terms of 10 to 15 years. Additionally, they company has several customer supply contracts within the Equipment and Energy segment with contract terms that are primarily 5 to 10 years. Under those contracts, the Company has built a facility on land owned by the customer, and is essentially a de-facto monopoly in the specific geographic area for that customer.

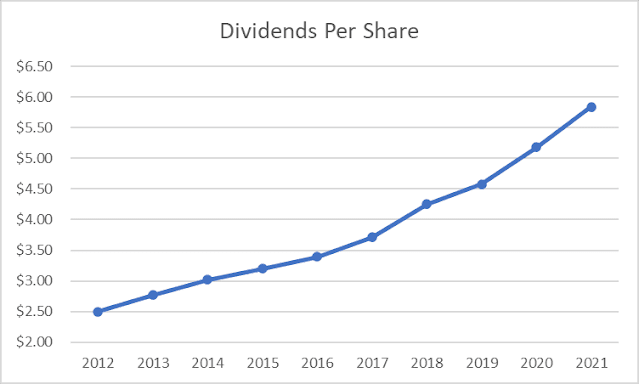

The annual dividend payment has increased by 11.10% per year over the past decade.

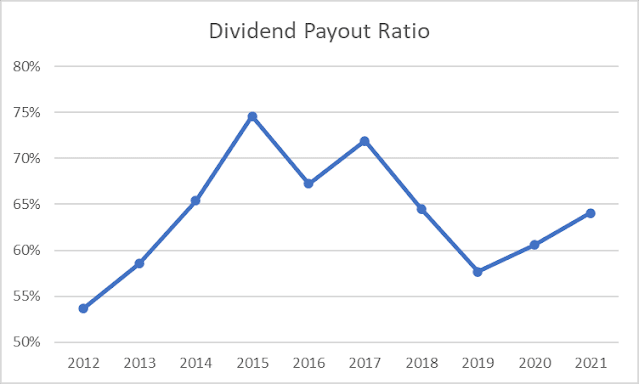

The dividend payout ratio increased from 54% in 2012 to 75% in 2015, before gradually decreasing back to 64% in 2021. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

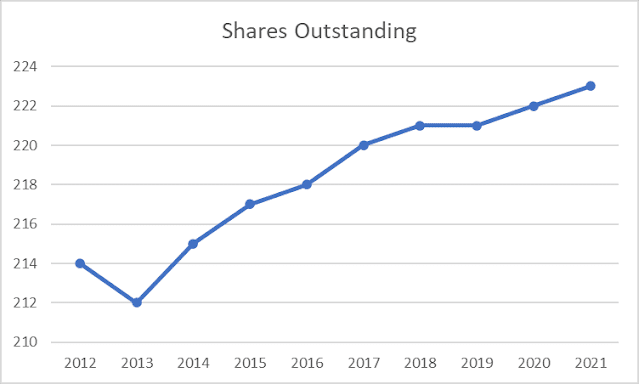

The number of shares outstanding has been growing at a snail pace. In general, you want to see shares outstanding flat or decreasing.

The stock is selling for 25.45 times forward earnings and yields 2.48%.