The privacy of our visitors to Dividend Growth Investor is important to us.

At Dividend Growth Investor, we recognize that privacy of your personal information is important. Here is information on what types of personal information we receive and collect when you use visit Dividend Growth Investor, and how we safeguard your information. We never sell your personal information to third parties.

Log Files As with most other websites, we collect and use the data contained in log files. The information in the log files include your IP (internet protocol) address, your ISP (internet service provider, such as AOL or Shaw Cable), the browser you used to visit our site (such as Internet Explorer or Firefox), the time you visited our site and which pages you visited throughout our site.

Cookies and Web Beacons. We do use cookies to store information, such as your personal preferences when you visit our site. This could include only showing you a popup once in your visit, or the ability to login to some of our features, such as forums. We also use third party advertisements on Dividend Growth Investor to support our site.

Some of these advertisers may use technology such as cookies and web beacons when they advertise on our site, which will also send these advertisers (such as Google through the Google AdSense program) information including your IP address, your ISP , the browser you used to visit our site, and in some cases, whether you have Flash installed. This is generally used for geotargeting purposes (showing New York real estate ads to someone in New York, for example) or showing certain ads based on specific sites visited (such as showing cooking ads to someone who frequents cooking sites).

We use third-party advertising companies to serve ads when you visit our website. These companies may use information (not including your name, address, email address, or telephone number) about your visits to this and other websites in order to provide advertisements about goods and services of interest to you. If you would like more information about this practice and to know your choices about not having this information used by these companies, click here.

Beginning April 8, 2009, Google advertising, as a third party vendor, will introduce Interest-based advertising that allows advertisers to show ads based on a user's previous interactions with them. To develop interest categories, Google will use the DoubleClick DART cookie. Google's use of the DART cookie enables it to serve ads to your users based on their visit to your sites and other sites on the Internet. Users may opt out of the use of the DART cookie by visiting the Google ad and content network privacy policy.

You can chose to disable or selectively turn off our cookies or third-party cookies in your browser settings, or by managing preferences in programs such as Norton Internet Security. However, this can affect how you are able to interact with our site as well as other websites. This could include the inability to login to services or programs, such as logging into forums or accounts.

Update: 8/11/2015

USES OF INFORMATION COLLECTED

(a) COMPANY USE OF INFORMATION

We may use Contact Data to send you information about our company or our products or services, or promotional material from some of our partners, or to facilitate the renewal of your subscription, or to improve our Site, or to contact you when necessary. We may use your Demographic Data to customize and tailor your experience on the Site; displaying content that we think you might be interested in and according to your preferences.

We may also use Contact Data for lead generation purpose by sending you information about products or services, or promotional material of other third party companies.

We only collect but will not use your Financial Data for any purpose. Our third party business partner will use your Financial Data to process your credit card payment.

(b) SHARING OR TRANSFERRING OF PERSONAL INFORMATION

By voluntarily registering and agreeing to (checked box opting into receiving marketing during registration) you are giving us your express consent to share your Personal Information with third parties in the ways described in this Privacy Policy.

We may share Demographic Data with advertisers and other third parties.

We may also share Contact Data with our business partners who assist us by performing core services (such as hosting, billing, fulfillment, or data storage and security) related to our operation of the Site.

When you provide us with your Financial Data, it will immediately be transferred to and stored with our third party payment-processing partner (i.e. Paypal). We will not retain any of your Financial Data in our database.

We maintain a procedure for you to review and request changes to your Personal Information; this procedure is described in Section 3.1, below.

You acknowledge that once your Personal Information is shared with or transferred to third parties as provided herein, the use of your Personally Information will then be governed by the privacy policies of those third parties and is not subject to our control. If contacted by those third parties, you should directly inquire them about the use of your Personal Information by them.

(c) USER CHOICE REGARDING COLLECTION, USE, AND DISTRIBUTION OF PERSONAL INFORMATION

You may choose not to provide us with any Personal Information. In such an event, you can still access and use much of the Site; however you will not be able to access and use those portions of the Site that require your Personal Information.

PRIVACY POLICIES AND DATA COLLECTION AT THIRD PARTY SITES

Except as otherwise discussed in this Privacy Policy, this document only addresses the use and disclosure of information we collect from you. Other sites accessible through our site have their own privacy policies and data collection, use and disclosure practices. Please consult each site's privacy policy. We are not responsible for the policies or practices of third parties. Additionally, other third-party companies which place advertising on our site may collect information about you when you view or click on their advertising through the use of their cookies or other tracking technologies, which may include delivering targeted advertisements and marketing messages based upon the third party websites that you visit, or other purposes. We cannot control this collection of information and are not responsible for the privacy policies and data collection, use and disclosure practices of these third party advertisers. You should contact these third party advertisers directly if you have any questions about their use of the information that they collect from you. Google/DoubleClick DFP is our third party ad server. If you would like to know more about their information gathering practices and "opt-out" procedures, please see http://www.google.com/policies/technologies/ads/

Also, if you would like more information about this practice and to know your choices about not having this information used by these companies, please see: http://www.networkadvertising.org/consumer/opt_out.asp

Thursday, January 31, 2008

Tuesday, January 29, 2008

An alternative strategy to covered calls

Instead of selling covered calls, I actually am considering selling put options on stocks for some extra income, which could work in some situations. First, when you are selling a naked put you are obligated to buy the stock from the put buyer, who has the right, but not the obligation to sell it to you at a predetermined strike price. If you invest a certain amount of funds each month into stocks for example, you are basically always buying at the market price. If you always invest 120-125 dollars per month in DIA you are trying to buy one share per month at a time, rather than all 12 at once, by using the power of dollar cost averaging. In this situation, if you sell a naked put on DIA at an in the money strike of say 122, you would be paid $3.10 for the obligation to buy DIA at $122. If DIA does fall below 122 at expiration, you most probably would have to buy it at the strike price. With this strategy you bring your cost basis significantly below the current market price of 122.19 to an actual $118.90 if your option is exercised. Since stocks have historically always been in a bull market over the past 200 years, it makes sense to me to buy stocks that have shown some weakness, get dividend payments and live the good life.

The shortfall in this strategy is that you are only buying stocks which are showing weakness. In a strong market you will miss on potential gains, because you are only buying a stock that has fallen below your strike price and thus there’s no guarantee that that you will receive the lower cost basis. In weak markets you will be able to buy your stock at a lower price, but you will see your stock dive further down. Thus you might have been better off postponing your buy.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

- Covered Call Options Strategy for cutting losses

The shortfall in this strategy is that you are only buying stocks which are showing weakness. In a strong market you will miss on potential gains, because you are only buying a stock that has fallen below your strike price and thus there’s no guarantee that that you will receive the lower cost basis. In weak markets you will be able to buy your stock at a lower price, but you will see your stock dive further down. Thus you might have been better off postponing your buy.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

- Covered Call Options Strategy for cutting losses

Monday, January 28, 2008

Covered Calls for additional income

A friend of mine suggested to me to sell covered calls on the dividend stocks that I own, in order to increase my income. Basically that means that I will sell an out of the money call option on a stock I already own at a given strike above the current price and collect the premium. This does sound appealing, because theoretically I could get two passive income streams from one stock. There are some risks with this strategy though, that make it less appealing to me:

First, when you sell an out of the money covered call option, you are basically betting that your stock would not increase above the strike price at which you’ve written the options. Thus if I owned Pepsi at $69, share and I sell a February covered call at the $75 strike; I would be betting that the price of Pepsi would not increase over $75 over the period. And I always expect that my stocks would go through the roof in any period, otherwise I wouldn’t have bought them in the first place.

Second, if the price rises to 80, I would not be able to participate in the upside gains above 75, because I am obligated to sell it to the call buyer to whom I wrote the call option to. The only scenario in which I will keep the stock and the premium is when the stock price does not increase above $75. This strategy seems inferior because it assumes that investors could time the market by betting whether or not the stock would be above/below the strike price at expiration. Studies have shown that investors are pretty bad at timing the markets, because the majority always seems to be selling at the bottoms and buying at the top. It also seems inferior because you are limiting your upside, and leaving your downside wide open. You are selling your rising stocks and keeping your losers, while earning some income in the process, which in reality is eroding your capital gains. The psychological weak points of this strategy is that most investors always believe that their stocks would be rising over time, so betting against your own portfolio in terms of covered call selling seems counterintuitive.

If I were simply interested in income, I would put all of my money in a bond yielding me 5% annually and simply compound the interest. I am in this game not only for the income potential but also for the capital gains. Thus I am not a believer in the covered call strategy. If I thought that my stock would not increase a lot, then I would sell it and buy a stock that I believe would increase a lot. Tomorrow I would write about another options strategy for generating income.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

- Covered Call Options Strategy for cutting losses

First, when you sell an out of the money covered call option, you are basically betting that your stock would not increase above the strike price at which you’ve written the options. Thus if I owned Pepsi at $69, share and I sell a February covered call at the $75 strike; I would be betting that the price of Pepsi would not increase over $75 over the period. And I always expect that my stocks would go through the roof in any period, otherwise I wouldn’t have bought them in the first place.

Second, if the price rises to 80, I would not be able to participate in the upside gains above 75, because I am obligated to sell it to the call buyer to whom I wrote the call option to. The only scenario in which I will keep the stock and the premium is when the stock price does not increase above $75. This strategy seems inferior because it assumes that investors could time the market by betting whether or not the stock would be above/below the strike price at expiration. Studies have shown that investors are pretty bad at timing the markets, because the majority always seems to be selling at the bottoms and buying at the top. It also seems inferior because you are limiting your upside, and leaving your downside wide open. You are selling your rising stocks and keeping your losers, while earning some income in the process, which in reality is eroding your capital gains. The psychological weak points of this strategy is that most investors always believe that their stocks would be rising over time, so betting against your own portfolio in terms of covered call selling seems counterintuitive.

If I were simply interested in income, I would put all of my money in a bond yielding me 5% annually and simply compound the interest. I am in this game not only for the income potential but also for the capital gains. Thus I am not a believer in the covered call strategy. If I thought that my stock would not increase a lot, then I would sell it and buy a stock that I believe would increase a lot. Tomorrow I would write about another options strategy for generating income.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

- Covered Call Options Strategy for cutting losses

Saturday, January 26, 2008

What’s a passive income from dividends?

Among the popular internet media there’s a widespread belief that passive income is income which you receive without even moving a finger. Although the term passive income implies that you simply receive checks or that the money is simply directly deposited into your bank account without any effort on your side, I think that that’s not the case in reality. An example of passive income that comes to mind is interest on Bonds that is paid to the holder at a fixed period. Other examples include royalties from music sales, which was created by artists long after their bands have fallen off the charts, income from rental properties, income from online advertising and income from dividends.

From these examples it is visible that passive income is a direct result of some economic activity or work, which created some good/service which society is still willing to reward the holder of the idea long into the future. If you buy stock in a corporation, you increase the liquidity of its shares, making it easier for the company to sell stock in the future to its shareholders. This liquidity also provides an incentive to shareholders to keep their wealth invested in stocks, because they would always be able to transform their paper wealth into dollars and consumption. Investors are further rewarded for holding stocks which reward them with dividend payments paid 4 times per year in the US. Some foreign corporations though, pay their dividends once a year, which provides an uneven stream of income for their shareholders, unlike US ones.

Studies have shown that dividend paying companies tend to outperform the general market over time. Thus I believe that a strategy of investing in stocks that regularly distribute their earnings to shareholders will provide one with a good return over time. Companies that pay dividends show that they care about their owners and have a good corporate policy toward them. Companies that not only pay dividends every year, but also strive at increasing them every year show confidence in the superiority of their business model relative to other industries. An investor, who puts his money to work in such a stock, will be rewarded with an ever increasing stream of income, which would compound at faster rates than simply putting ones money in a bank account.

Thus I believe that building a well-diversified portfolio of companies who have a history of consistently increasing their dividends over time is a good extra source of income for many people. It takes very little time to set up and implement, and can lead to very good returns in the future by reinvesting and compounding your dividends and spreading your buys over time.

I have attached a chart showing the dividend payments over time for Pepsi Co since 1977. If you had invested $1,000 back in those days into Pepsi Stock, your annual dividend income would have risen from $34 during your first year as a shareholder to $1071 in 2007. Furthermore, if you had simply reinvested these dividends every year, your initial $1000 investment would have grown to over $116,000. The main reason for this high number is dividend reinvestment - if you had spent your dividend payments each year instead of reinvesting them into company stock your investment would have been worth only $51,000. In addition, if you had kept on reinvesting your quarterly dividend payments, your annual income would have increased to over $2,000 in 2007. Of course this sort of capital gains might not be replicated in the future but one thing is for sure – if the company keeps expanding and raising its dividend payment year in and year out, I would be its stockholder. It’s very nice to have your salary increased every year. That’s what dividend aristocrats like Pepsi provide to their shareholders in terms of payments.

From these examples it is visible that passive income is a direct result of some economic activity or work, which created some good/service which society is still willing to reward the holder of the idea long into the future. If you buy stock in a corporation, you increase the liquidity of its shares, making it easier for the company to sell stock in the future to its shareholders. This liquidity also provides an incentive to shareholders to keep their wealth invested in stocks, because they would always be able to transform their paper wealth into dollars and consumption. Investors are further rewarded for holding stocks which reward them with dividend payments paid 4 times per year in the US. Some foreign corporations though, pay their dividends once a year, which provides an uneven stream of income for their shareholders, unlike US ones.

Studies have shown that dividend paying companies tend to outperform the general market over time. Thus I believe that a strategy of investing in stocks that regularly distribute their earnings to shareholders will provide one with a good return over time. Companies that pay dividends show that they care about their owners and have a good corporate policy toward them. Companies that not only pay dividends every year, but also strive at increasing them every year show confidence in the superiority of their business model relative to other industries. An investor, who puts his money to work in such a stock, will be rewarded with an ever increasing stream of income, which would compound at faster rates than simply putting ones money in a bank account.

Thus I believe that building a well-diversified portfolio of companies who have a history of consistently increasing their dividends over time is a good extra source of income for many people. It takes very little time to set up and implement, and can lead to very good returns in the future by reinvesting and compounding your dividends and spreading your buys over time.

I have attached a chart showing the dividend payments over time for Pepsi Co since 1977. If you had invested $1,000 back in those days into Pepsi Stock, your annual dividend income would have risen from $34 during your first year as a shareholder to $1071 in 2007. Furthermore, if you had simply reinvested these dividends every year, your initial $1000 investment would have grown to over $116,000. The main reason for this high number is dividend reinvestment - if you had spent your dividend payments each year instead of reinvesting them into company stock your investment would have been worth only $51,000. In addition, if you had kept on reinvesting your quarterly dividend payments, your annual income would have increased to over $2,000 in 2007. Of course this sort of capital gains might not be replicated in the future but one thing is for sure – if the company keeps expanding and raising its dividend payment year in and year out, I would be its stockholder. It’s very nice to have your salary increased every year. That’s what dividend aristocrats like Pepsi provide to their shareholders in terms of payments.

Friday, January 25, 2008

Account Opening Bonus for OptionsXpress

Optionsxpress has a $100 bonus for new customers that open an account with them and deposit at least $500 by March 31, 2008. That's what their website says:

You need to have your account open for at least 6 months and your account balance should not fall below $500 unless you have trading losses.

http://www.optionsxpress.com/promos/free.aspx

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

To receive $100 bonus, account must be funded with at least $500 cash or

securities transferred from a brokerage firm other than optionsXpress. $100

bonus will be deposited into the new optionsXpress account by April 30,

2008.

You need to have your account open for at least 6 months and your account balance should not fall below $500 unless you have trading losses.

http://www.optionsxpress.com/promos/free.aspx

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Thursday, January 24, 2008

Some Charts to watch

Even though this blog focuses on achieving long-term dividend income, I think that sometimes it might be ok to satisfy my readers who have a shorter term objective at trading/investing than me. For a short-term trader it is imperative to look at charts in order to analyze the situation tick by tick, trade by trade. I myself used to focus on very short term trends ( 1-2 days) before I embraced the dividend growth strategy that I write about in this blog. If you look at the daily charts of SPY and DIA, two well-known exchange traded funds that follow the S&P 500 and Dow Joned 30 indices, you will notice the smaller than average trading range today. It looks as if the market is at crossroads right now - trying to decide whether to go up, continue moving down or just move sideways for a while.

If I were short-term trading this market, my orders for tomorrow for SPY would be:

Buy Stop X amount of shares @ 135.47 , stop loss @ 133.30 and trail your stop loss upward for every penny that the ETF moves in your direction.

Sell Short Stop X amount of shares @ 133.30 , stop loss @135.47 and and trail your stop loss downward for every penny that the ETF moves in your direction.

The orders for DIA would be:

Buy Stop X amount of shares @ 123.93 , stop loss @ 122.25and trail your stop loss upward for every penny that the ETF moves in your direction.

Sell Short Stop X amount of shares @ 122.25 , stop loss @ 123.93and and trail your stop loss downward for every penny that the ETF moves in your direction.

Sell Short Stop X amount of shares @ 122.25 , stop loss @ 123.93and and trail your stop loss downward for every penny that the ETF moves in your direction.

If SPY or DIA open tomorrow @ 9:30 AM ET above 135.47 and 123.93 respectively, then the long side of the trade should not be implemented, but the short side could still be done. If SPY and DIA open tomorrow morning below 133.30 and 122.25 you should not implement the short side of the trade, but the long could still be done.

Also, if one of the trades is triggered and then stopped out, you should take the second trade. The worst thing that could happen is a 2% loss.

You should try not to risk more than 1% of your capital on SPY or DIA ( assuming that you take only one of the trades). Therefore if your capital is 25,000 and you were trading DIA you shouldn't buy or sell short no more than 148 shares; if you decide to trade SPY you should trade no more than 115 shares. (115 shares X $2.17 risk per share =almost 250, which is exactly 1% of your account balance).

Anyways, enough about our short-term trader audience. Good luck tomorrow everyone!

My Current Watchlist

The two lists that I am concentrating right now is the S&P 500 Dividend Aristocrats and the S&P High Yield Dividend Aristocrats Index. I created custom lists in Yahoo! Finance in order to summarize the two groups of dividend achievers by a variety of criteria such as Symbol, Yield, P/E , Div/Shr, Last Price,EPS (ttm) ,PEG Ratio ,Dividend Payout, 5 and 10 year dividend growth rates. What I did was first exclude any stocks which had a dividend payout ratio of more than 50%. That gives me some reasonable assurance that the company is less likely to cut its dividends. I also look at P/E ratios, since I do not want to overpay for a company. Anything with a P/E of over 20 is out of my watchlist. I also look for the PEG ratio but just to find stocks which might be expensive in terms of their growth prospects. A third thing that I look for is a dividend yield of at least 2%, which is a little bit over than the current yield of 1.89% that SPY is rewarding its shareholders. The last but not least criteria that I screen for is the 5 and 10 year dividend growth ratios. I am looking for an average annual dividend growth of at least 5% over the past 5 and 10 years. The reason why I selected dividend yield in the end is because I want to decrease to a minimum the rush to buy a stock that simply increased its dividend for whatever reason, whose fundamentals cannot support any

significant further increases in the dividend payments

Based off of this screen, my two stock lists to follow are those (as of close of business yesterday): (opens in new window)

ABM BUD CB CINF CLX DOV EMR FDO GCI GWW JNJ MMM MTB ROH RPM SNV VAL VFC WL MHP NUE PEP PG SHW

I would continue screening for potential stocks to add to my buy watchlist on a weekly basis. I might add or remove stocks from my watchlists depending on how undervalued/overvalued I perceive them to be. If I stock in which I have a position drops off my buy watchlist, I would keep holding it, but I won’t be adding to that position until the technicals and the fundamentals match my criteria.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

significant further increases in the dividend payments

Based off of this screen, my two stock lists to follow are those (as of close of business yesterday): (opens in new window)

ABM BUD CB CINF CLX DOV EMR FDO GCI GWW JNJ MMM MTB ROH RPM SNV VAL VFC WL MHP NUE PEP PG SHW

I would continue screening for potential stocks to add to my buy watchlist on a weekly basis. I might add or remove stocks from my watchlists depending on how undervalued/overvalued I perceive them to be. If I stock in which I have a position drops off my buy watchlist, I would keep holding it, but I won’t be adding to that position until the technicals and the fundamentals match my criteria.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Wednesday, January 23, 2008

My Goals

My personal goal is to achieve a significant amount of dividend income to cover my expenses. I would achieve that by investing an equal portion of my regular paycheck every month and reinvesting the dividend income. I would try to focus on high-yielding stocks, which increase their dividend payments over time. I try to cut my trading costs by switching to Zecco, which doesn’t charge you a commission once your account balance is over $2,500 and you don’t make more than 10 trades per month. Achieving a sufficient amount in dividend income is feasible depending on the amount of money you have invested as well as the yield on invested capital that you can achieve. For example, if the amount I need is $8,000/year in 6 years, it would be dependent on time I have to invest and amount I have to invest. Assuming that I have about $100,000 invested in 6 years, I would have to own assets yielding/earning 8% annually. If I have $200,000 invested at the time I would only need a 4% annual yield. I believe that this is a very conservative goal since I will have two powerful allies that would help me reach this goal - dollar cost averaging and dividend compounding. I won't put the money into a 401K or a ROTH IRA, because I plan on using them in a few years. If I put all the money for my dividend growth strategy in a retirement account, i won't be able to use the passive income when I want or need it.

Currently I am also contributing at a 401k plan though, which matches 100% of the first 5% of my income that I contribute. I am moderately diversified – 95% stocks and 5% bonds. 75% of my portfolio is invested in SP500, 10% in MSCI EAFE, 10% in Russell 2000. 2.5% of my 401K is invested in high-yielding bonds and the other 2.5% is invested in corporate bonds. I would continue contributing to my retirement accounts as well, which would grow tax free for 30 years or more.

I also have the option of contributing up to 25 % of my income into my employer stock participation plan, which allows me to buy company stock at a 10% discount and there’s no minimum holding period. I could simply elect to contribute 25% of my paycheck to the plan each quarter, buy the stock at quarter end and achieve an 11% quarterly return on investment!

As of now I have over 80% of my assets invested in certificates of deposit earning me around 5% per year. As they start maturing I would start investing these funds into dividend stocks that fit my buy criteria. I currently earn around $1,000 annually from interest income from these CD’s. The thing that turns me off from CD’s is the taxation of CD income as ordinary income versus the 15% tax rate on dividends. In addition, my stock investments would provide me with an income stream that is growing without having to reinvest any of my payments (in case I have to live off of them). I plan on retiring in a few years and moving to a beautiful country in East Europe, which recently joined the European Union. A dollar in Eastern Europe buys much more stuff and a dollar in US. The average salary is about $500/month there, but rents in big cities might go as high as my rent in the Midwest area.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Currently I am also contributing at a 401k plan though, which matches 100% of the first 5% of my income that I contribute. I am moderately diversified – 95% stocks and 5% bonds. 75% of my portfolio is invested in SP500, 10% in MSCI EAFE, 10% in Russell 2000. 2.5% of my 401K is invested in high-yielding bonds and the other 2.5% is invested in corporate bonds. I would continue contributing to my retirement accounts as well, which would grow tax free for 30 years or more.

I also have the option of contributing up to 25 % of my income into my employer stock participation plan, which allows me to buy company stock at a 10% discount and there’s no minimum holding period. I could simply elect to contribute 25% of my paycheck to the plan each quarter, buy the stock at quarter end and achieve an 11% quarterly return on investment!

As of now I have over 80% of my assets invested in certificates of deposit earning me around 5% per year. As they start maturing I would start investing these funds into dividend stocks that fit my buy criteria. I currently earn around $1,000 annually from interest income from these CD’s. The thing that turns me off from CD’s is the taxation of CD income as ordinary income versus the 15% tax rate on dividends. In addition, my stock investments would provide me with an income stream that is growing without having to reinvest any of my payments (in case I have to live off of them). I plan on retiring in a few years and moving to a beautiful country in East Europe, which recently joined the European Union. A dollar in Eastern Europe buys much more stuff and a dollar in US. The average salary is about $500/month there, but rents in big cities might go as high as my rent in the Midwest area.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Tuesday, January 22, 2008

The Fed Cut Rates by 0.75% this morning!

The Federal Reserve Cut its rates by 0.75% today. I think that we have a pretty good opportunity to go long the market today, if the S&P 500 exceeds its 30 minuite high, with a stop loss at the 30 min low. However you should do this only for a trade and if entered into the trade, please trail your stop to cut your losses and/or protect some of any profits. Exit at the close if you are not stopped out. I expect further turbulence in the markets. Unfortunately fixed income is not going to yield as much so certificates of deposit would yield much less. I normally buy my CD's from Bank Midwest, which offers a competitive yield on their 9 month certificates.

The Federal Reserve Cut its rates by 0.75% today. I think that we have a pretty good opportunity to go long the market today, if the S&P 500 exceeds its 30 minuite high, with a stop loss at the 30 min low. However you should do this only for a trade and if entered into the trade, please trail your stop to cut your losses and/or protect some of any profits. Exit at the close if you are not stopped out. I expect further turbulence in the markets. Unfortunately fixed income is not going to yield as much so certificates of deposit would yield much less. I normally buy my CD's from Bank Midwest, which offers a competitive yield on their 9 month certificates.Monday, January 21, 2008

$50 Sharebuilder Account Opening Bonus

Sharebuilder has a $50 account opening bonus, if you open an account with them and do one purchase of a security. The disclaimer says that they will deposit the bonus amount in 4 weeks after you make your first purchase. You have to be a new account holder to qualify though. The offer does not apply to IRA or Educational Savings Accounts.

You can find the link here. Promotional code is SHARE50

Full Disclosure: I won't earn anything form that offer.

You can find the link here. Promotional code is SHARE50

Full Disclosure: I won't earn anything form that offer.

How I outperformed the market and how you can outperform S&P 500 in 2008

After I graduated from college in May 2007, I started interviewing and finally got a real job in July. I never had any credit card debt or any student loans since I worked 20-30 hours/week during school, 70-80 hours/week during breaks, kept good GPA’s, campus involvement, won some scholarships (I didn’t have a full ride though) but most importantly lived frugally.

My current employer pays me well, and I have all sorts of benefits. The problem for me was that I didn’t spend all the money that I earn, since I learned in college to live frugally. I wanted to buy index ETF’s like SPY, VEU, CWI or EEM. However, that involved risk, and after 4 years of rising stock prices, financial markets looked toppy. In addition the news always talked about how the housing market is crashing. Thus I started putting all my money in 9 Month Certificates of Deposit, yielding 5 – 5.3% annually. I also put 5 % of my income in 401k, since my employer provides me with a 100% match on that amount. I bought my first CD on July 27, and I bought my last CD on January 14. In the meantime the S&P 500 has started falling a lot. It’s currently trading at 15 month lows. It’s also down 9.7% since the start of the year. So once my CD’s start maturing in April and beyond, and the market being pushed down by news about recession, housing bubble etc, I would be in a good position to buy good dividend paying stocks which have a history if consistently increasing their payments. I would write more on my watch list later on.

The funniest thing is that if were a fund manager/ stock investor who didn’t invest his/her money until now ( instead of doing his/her purchases at year-end 2007) you have a risk-free way of OUTPERFORMING S&P 500 in 2008 by a whopping 10% just by putting your whole portfolio in SPY and forgetting about it. In addition to that, you would still be able to outperform the market on average by 1 % point over the next 10 years!

Unfortunately though, waiting for the market to fall below its year-end close at the beginning of a new year is not a good long-term strategy. If you participated in this sort of market timing, you would have missed some big moves in the market like the one in 1995. Fixed Income securities like CD’s, bonds and money market also have lower long-term returns, compared to stocks. Even if you buy SPY at current prices, you would outperform the market in 2008, but there’s no guarantee that you will make money. The market could still go lower. So what should an investor do? Maybe you could start building positions in companies which would not suffer significant blows in their financial position from a recession. Furthermore the management of these companies should reward its shareholders by consistently distributing increased dividend payments year after year, supported by increase in earnings. If you get a good yield on your stocks and you are confident that the payment will increase over time, then you should put money consistently into those names. Through the power of dollar-cost averaging and compounding, you will come out ahead of the game in the end with a pretty decent passive dividend income.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

My current employer pays me well, and I have all sorts of benefits. The problem for me was that I didn’t spend all the money that I earn, since I learned in college to live frugally. I wanted to buy index ETF’s like SPY, VEU, CWI or EEM. However, that involved risk, and after 4 years of rising stock prices, financial markets looked toppy. In addition the news always talked about how the housing market is crashing. Thus I started putting all my money in 9 Month Certificates of Deposit, yielding 5 – 5.3% annually. I also put 5 % of my income in 401k, since my employer provides me with a 100% match on that amount. I bought my first CD on July 27, and I bought my last CD on January 14. In the meantime the S&P 500 has started falling a lot. It’s currently trading at 15 month lows. It’s also down 9.7% since the start of the year. So once my CD’s start maturing in April and beyond, and the market being pushed down by news about recession, housing bubble etc, I would be in a good position to buy good dividend paying stocks which have a history if consistently increasing their payments. I would write more on my watch list later on.

The funniest thing is that if were a fund manager/ stock investor who didn’t invest his/her money until now ( instead of doing his/her purchases at year-end 2007) you have a risk-free way of OUTPERFORMING S&P 500 in 2008 by a whopping 10% just by putting your whole portfolio in SPY and forgetting about it. In addition to that, you would still be able to outperform the market on average by 1 % point over the next 10 years!

Unfortunately though, waiting for the market to fall below its year-end close at the beginning of a new year is not a good long-term strategy. If you participated in this sort of market timing, you would have missed some big moves in the market like the one in 1995. Fixed Income securities like CD’s, bonds and money market also have lower long-term returns, compared to stocks. Even if you buy SPY at current prices, you would outperform the market in 2008, but there’s no guarantee that you will make money. The market could still go lower. So what should an investor do? Maybe you could start building positions in companies which would not suffer significant blows in their financial position from a recession. Furthermore the management of these companies should reward its shareholders by consistently distributing increased dividend payments year after year, supported by increase in earnings. If you get a good yield on your stocks and you are confident that the payment will increase over time, then you should put money consistently into those names. Through the power of dollar-cost averaging and compounding, you will come out ahead of the game in the end with a pretty decent passive dividend income.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Sunday, January 20, 2008

A comparison of investing in high-yield, low dividend growth stock versus investing in a low-yield, high dividend growth stock without capital gains

I was asked before about the reasoning behind my statement that I would buy a stock whose dividend is increasing even by one percentage point per year, if it has a high yield, rather than invest in stocks which increase their dividend payment by at least 10% per year. To answer this question, lets me walk you through my calculations:

Let’s say that you have 2 stocks- A and B in each of which we invest $100,000. We assume that both stocks will always trade at $10 for simplicity sake. Stock A is yielding 5% per year (50 cents per share), while Stock B is yielding 2% (20 cents per share). The dividend growth in Stock A is a meager 1%, while Stock B’s dividend is growing at 5% annually. We will look at two outputs – total return and changes in annual income. It would take stock B 24 years to reach the same annual income level as stock A. In addition, it would take stock B around 40 years to achieve the same total dollar return as stock A. If however we had a growth stock C, which was yielding .5 % at the start of the experiment, and whose dividend was growing at 10% annually, it would take the annual income around 27 years to reach Stock A’s dividend income. It would also take around 42 years for the total dollar return of Stock C to reach the total dollar return of Stock A. I have also included a $100,000 investment in bonds, which yield 6% every year.

The return from the invested capital though, would have been increasing substantially over time assuming that we didn’t reinvest our dividends back into our stocks. After 10 years the yield on cost for Stock A is 5.5%, Stock B is 3.3% and Stock C is 1.3%. After 10 more years stocks A, B and C are yielding 6.1%, 5.3% and 3.4%. An investor, who simply purchased bonds, would have been making the same 6% over and over. I am attaching my spreadsheet below. This file is for informational purposes only; I just tried to make my point that you have to not only buy a stock which has a high dividend growth rate, but also a one which has a pretty decent yield. A major limitation of this analysis was that I assumed that stocks would not realize any capital gains over the period; that’s why the long-term results of Stocks A, B and C are almost identical to long-term results for Bonds. However it shows you that if you reinvest dividends, stocks achieve a higher compounding power than bonds.

You can see the file here or here.

Let’s say that you have 2 stocks- A and B in each of which we invest $100,000. We assume that both stocks will always trade at $10 for simplicity sake. Stock A is yielding 5% per year (50 cents per share), while Stock B is yielding 2% (20 cents per share). The dividend growth in Stock A is a meager 1%, while Stock B’s dividend is growing at 5% annually. We will look at two outputs – total return and changes in annual income. It would take stock B 24 years to reach the same annual income level as stock A. In addition, it would take stock B around 40 years to achieve the same total dollar return as stock A. If however we had a growth stock C, which was yielding .5 % at the start of the experiment, and whose dividend was growing at 10% annually, it would take the annual income around 27 years to reach Stock A’s dividend income. It would also take around 42 years for the total dollar return of Stock C to reach the total dollar return of Stock A. I have also included a $100,000 investment in bonds, which yield 6% every year.

The return from the invested capital though, would have been increasing substantially over time assuming that we didn’t reinvest our dividends back into our stocks. After 10 years the yield on cost for Stock A is 5.5%, Stock B is 3.3% and Stock C is 1.3%. After 10 more years stocks A, B and C are yielding 6.1%, 5.3% and 3.4%. An investor, who simply purchased bonds, would have been making the same 6% over and over. I am attaching my spreadsheet below. This file is for informational purposes only; I just tried to make my point that you have to not only buy a stock which has a high dividend growth rate, but also a one which has a pretty decent yield. A major limitation of this analysis was that I assumed that stocks would not realize any capital gains over the period; that’s why the long-term results of Stocks A, B and C are almost identical to long-term results for Bonds. However it shows you that if you reinvest dividends, stocks achieve a higher compounding power than bonds.

You can see the file here or here.

My Strategy

My strategy involves buying companies which have a history of consistently increasing their dividend payments going back over as many years as possible . Depending on the period that you are focusing one there's not a lot of companies that might fit your criteria. S&P has several lists which are worth focusing on - companies which have consistently increased their dividend over the past 10 years, S&P Dividend Aristocrats and S&P high-yield Dividend Aristocrats. The positive thing about the last two lists is that they show you stocks that have raised their dividends consistently over the past 25 years! Remember i do not just focus on high-yielding stocks. A stock which shows you a 10% dividend yield when the average yield out there is 2% is most likely a stock, for which the market is telling you that there is a very high chance that the dividend payment would be cut and your yield would decrease. I would rather buy a stock that pays me around 2-3% currently, at a time when fixed income can provide me with a 4.5% - 5.00% yield, BUT which would increase its dividend payments in the future.

There are other lists of stocks which are considered dividend achievers. Another one worth focusing on is the Mergent's Dividend Achievers 50 and High-Growth Rate Dividend Achievers. The issue with those lists lies in the fact that it gives you only companies which have raised their dividend at least over the past 10 years. There are at least 300 such companies in the US currently, so for a small investor like me, this is a pretty big universe of stocks. The S&P Dividend Aristocrats and the High-Yield Dividend Aristocrats on the other hand contain 50 or so stocks each, which is a more manageable list to follow.

In my strategy, I would focus on buying stocks which give you at least the same yield as the broad S&P500 index, as represented by SPY. Furthermore, i would give preference to the dividend aristocrats and the high-yield dividend aristocrats over the other dividend achievers. In addition, I will look for companies, whose dividend payout ratio does not exceed 55-60% at the time of purchase. I would also try to equally weight my purchases. So for example if I invest 100 dollars per week, and I have a list of 52 achievers that fit my criteria, i would buy a different stock each week in a given year. I will not re balance my portfolio though, since this will increase my trading costs; it also runs contrary to the old adage of "cut your losers and let your profits ride".

I will try to diversify across sectors, without being too overweight in a certain sector like financials or utilities, which could prove to be easier to say than achieve. I will also look for an average dividend growth of at least 3% (which is the average long-term inflation rate). However, I might consider buying any stock that shows a growing dividend, even by a single percent per year, provided that the company spots an above average yield. Even though the passive dividend income will rise much slower, your money will compound at a higher rate for a long period of time. A very good dividend stock candidate for purchase would be one showing an above average dividend growth as well as an above average yield.

I will try to diversify across sectors, without being too overweight in a certain sector like financials or utilities, which could prove to be easier to say than achieve. I will also look for an average dividend growth of at least 3% (which is the average long-term inflation rate). However, I might consider buying any stock that shows a growing dividend, even by a single percent per year, provided that the company spots an above average yield. Even though the passive dividend income will rise much slower, your money will compound at a higher rate for a long period of time. A very good dividend stock candidate for purchase would be one showing an above average dividend growth as well as an above average yield.

I would consider selling a stock once it starts decreasing dividends; I won't sell simply because a company whose stock I already own does not raise its dividend, but I might not add any more fresh money into this position.

My goal is to achieve an above average yield on cost in the future. For example if I had invested $1000 on Dec 31, 1989 in MO ( Altria ) you would have bought 24 shares and had a dividend income in 1990 of $35, and achieved a dividend yield of around 3.5%. If you held your stock until Dec 31, 2006, you would have had a dividend income for 2006 of $239 on 72 shares! That's an almost 24% annual yield. Your 24 shares would have turned into 72 shares worth $6179 at the end of 2006. Furthermore, if you had reinvested your dividends the $1000 investment in 1989 would have turned into $18,167!

Are Dividend ETF's for you?

There is a variety of ETF's out there that focus on many different dividend strategies including but not limited to domestic and international dividend achievers, high-growth dividend achievers, aristocrats and even dividend weighted baskets of stocks. While there seems to be an advantage for the small investor with several thousand dollars to invest in buying a predetermined basket of dividend stocks in terms of paying less commissions for buying one ETF, versus paying commissions on buying separately each and every stock in the index, there are disadvantages as well.

First of all some of these ETF's follow indexes which are updated only once an year. Thus, they might still be holding stocks which have failed to increase their dividend in the past year due to timing.

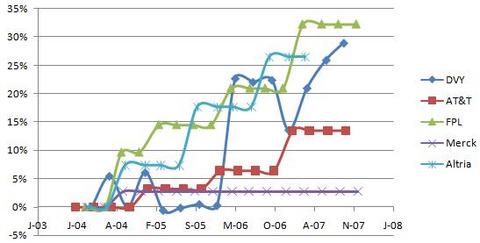

Second, you might not want to buy certain sectors which you perceive as having further downside possibility. A weak sectors which comes to mind right now is financials, which seems to have a higher than average sector-weight in the plethora of dividend ETF's like the DVY for example.

Third, these ETF's are weighted according to different formulas, which might add to or detract from performance. I myself am a firm believer in equal weighted investing, which outperforms the market by a little over large periods of time.

And fourth the dividends from these ETF's seem to be following an erratic pattern, rather than the stable and consistent growth that their individuals stock components should have been experiencing.

First of all some of these ETF's follow indexes which are updated only once an year. Thus, they might still be holding stocks which have failed to increase their dividend in the past year due to timing.

Second, you might not want to buy certain sectors which you perceive as having further downside possibility. A weak sectors which comes to mind right now is financials, which seems to have a higher than average sector-weight in the plethora of dividend ETF's like the DVY for example.

Third, these ETF's are weighted according to different formulas, which might add to or detract from performance. I myself am a firm believer in equal weighted investing, which outperforms the market by a little over large periods of time.

And fourth the dividends from these ETF's seem to be following an erratic pattern, rather than the stable and consistent growth that their individuals stock components should have been experiencing.

{kind=link}

{kind=link}

Saturday, January 19, 2008

Why dividends matter?

Jonathan from MyMoneyBlog had a pretty good article about why Dow Jones Industrials is not an accurate index to follow. He sites this research paper named The Dow Jones Industrial Average: The Impact of Fixing Its Flaws. Basically this paper shows that if dividends were included in the Dow Jones Industrials, its value would be around 250,000 points in 2000, versus the 9,000 it was trading in 1999!

It is commonly known that it took the market 25 years to recover from its 1929 peak and the Great Depression. However the inclusion of dividends in the index mitigates the effects of the Great Depression. A new all-time high is reached in January 1945 instead of November 1954 if dividends are included.

To summarize, dividends should be considered an important part of ones portfolio. Financial advisers normally tell you that when you retire, you would be taking a 4% withdrawal rate from your nest egg each year. However, if you can achieve at least a 4% yield, that grows each year to at least cover the rise in inflation you would be able to weather any short-term and long-term weakness in the stock market. I would not recommend having a huge portion of your long-term portfolio in bonds, which are normally sold to retirees as a "safe and reliable source of income". You do get a fixed payment every period or so, but the purchasing power of this payment declines over time. Thus a very good strategy over the long run is to create a diversified portfolio of stocks, that have shows consistency in raising their dividends year after year and which spot an attractive dividend yield.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

It is commonly known that it took the market 25 years to recover from its 1929 peak and the Great Depression. However the inclusion of dividends in the index mitigates the effects of the Great Depression. A new all-time high is reached in January 1945 instead of November 1954 if dividends are included.

To summarize, dividends should be considered an important part of ones portfolio. Financial advisers normally tell you that when you retire, you would be taking a 4% withdrawal rate from your nest egg each year. However, if you can achieve at least a 4% yield, that grows each year to at least cover the rise in inflation you would be able to weather any short-term and long-term weakness in the stock market. I would not recommend having a huge portion of your long-term portfolio in bonds, which are normally sold to retirees as a "safe and reliable source of income". You do get a fixed payment every period or so, but the purchasing power of this payment declines over time. Thus a very good strategy over the long run is to create a diversified portfolio of stocks, that have shows consistency in raising their dividends year after year and which spot an attractive dividend yield.

- I believe dividends matter, because companies that pay regular dividends tend to be in better financial health and produce sustained earnings and revenue growth.

- Dividends also help identify well-managed companies; every dividend declaration represents a promise by management and a vote of confidence by the board of directors in the company's leadership.

- Companies that consistently raise their dividend payouts also raise the bar on their own performance expectations.

- Shares of dividend-paying companies possess built-in value that makes them generally more resilient in down markets, with solid appreciation potential during earnings-driven market upturns — with less price volatility.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Why dividends?

I believe that creating a passive income stream through dividends is an achievable, intriguing and stimulating way to decrease my dependency on the salary income, which is over 95% of my income at the moment. The remaining 5% comes from interest income from CD's and my interest checking account at Schwab, credit card rewards and signing up for offers online. After doing some research, i have found that putting your money in bonds, cds and money market funds will only be enough to meet inflation and over long periods of time exceed it by a couple percentage points on average.

Stocks on the other hand offer you the best possible investment opportunity out there. Over 30-35% of stocks performance over the past 50 years has been attributed to dividends; the rest comes from capital gains. If you take a look at the S&P 500 from 1957- 2005, the dividends have grown on average of 5.3% per year for the index. A $1000 investment in the S&P500 in early 1957 would have provided you with an annual dividend income of about $40. In 2005 your dividend income would have grown to $610, assuming that you spent all your income. Furthermore your investment would have been worth over $32,000 by the end of 2007. With inflation assumed to be averaging around 3 - 4% per year, your investment in dividend paying stocks would provide you with an income that keeps its purchasing power year over year, which unlike fixed income securities, can also provide you with capital gains.

My strategy involves saving around half of my paycheck and investing it in the dividend achievers and high yield dividend achievers that show consistent increases in dividends over time and the ability to cover those dividends in the future. I will have my screening method and my goals for passive income on my next posts. I would also try to describe my current net worth, and how it is invested. I hope that this blog will serve as an inspiration for people and that it would change their financial lives for the better.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Stocks on the other hand offer you the best possible investment opportunity out there. Over 30-35% of stocks performance over the past 50 years has been attributed to dividends; the rest comes from capital gains. If you take a look at the S&P 500 from 1957- 2005, the dividends have grown on average of 5.3% per year for the index. A $1000 investment in the S&P500 in early 1957 would have provided you with an annual dividend income of about $40. In 2005 your dividend income would have grown to $610, assuming that you spent all your income. Furthermore your investment would have been worth over $32,000 by the end of 2007. With inflation assumed to be averaging around 3 - 4% per year, your investment in dividend paying stocks would provide you with an income that keeps its purchasing power year over year, which unlike fixed income securities, can also provide you with capital gains.

My strategy involves saving around half of my paycheck and investing it in the dividend achievers and high yield dividend achievers that show consistent increases in dividends over time and the ability to cover those dividends in the future. I will have my screening method and my goals for passive income on my next posts. I would also try to describe my current net worth, and how it is invested. I hope that this blog will serve as an inspiration for people and that it would change their financial lives for the better.

Relevant Articles:

- Dividend Aristocrats List for 2009

- Dividend Aristocrats

- Best Dividends Stocks for the Long Run

- Best High Yield Dividend Stocks for 2009

- Best CD Rates

Subscribe to:

Posts (Atom)