I use a few quantitative factors in my investing including streak of annual dividend increases, dividend payout ratios, growth in earnings per share, and P/E ratios. I also use qualitative factors such as moat, competitive position, industry, product or service stickiness etc.

However, a lot of factors behind successful investing are dependent on the conditions present at the time you place your hard earned capital at risk.

For example, different companies and industries are available on sale at different times. Back in 2017 and 2018, we had a lot of REITs selling off on fears that the economy is slowing down and interest rates are rising. We had the same fears in 2013 as well. As I write this article in the middle of 2019 however, I find REITs to be a little pricey. And by REITs I am thinking about the likes of Realty Income (O), National Retail Properties (NNN), W.P. Carey (WPC). You have to be very selective in order to uncover good values in REITs today, and make sure that these entities are not cheap for a reason. Value traps can be expensive.

At other times certain industries end up being disrupted, despite having a long history of success. The newspaper industry comes to mind for me. There used to be companies like Gannett (GCI), which had long histories of annual dividend increases, up until having to cut dividends around the time of the Global Financial Crisis.

I am using these two instances as examples that things are never the same when it comes to investing. You can do a great quantitative and qualitative analysis of a business but can still lose money if the conditions are not right. The same principles that may have worked between 1999 – 2009 may turn out to not work as well between 2010 – 2019. As a result, you should always have some margin of safety built into whatever investment model you follow. After all, things may change despite our best efforts in the investment selection process. This is why you should still have built in redundancies in place in order to survive to fight another day.

I cringe when someone states that their investing model is based on science. Past performance is not an indication of future results. Overly relying on past data can be costly, because the investment environment in the backtest was different than the investment environment when your money is on the line.

You do not want to have an investment model that is based purely on past data, without taking into consideration the current environment. For example, a lot of investors may see historical information from a mutual fund and estimate that the future returns may be similar. However, if they forget about taking historical performance in a context, and misunderstanding the changes in the investment environment, they may be in for a surprise. If that mutual fund returned 9%/year by buying and holding treasury bonds between 1980 and 2010, that may have been because it was easier to buy bonds yielding close to 9%/year at the time. However, with long-term treasuries yielding around 3%, it is highly unlikely that an investment in treasury bonds will generate more than 3%/year.

I also see it to a certain extent with some retirees who believe that it is possible to live off a certain percentage of their stock portfolios in retirement ( say 4%). However, their dataset included periods when the average dividend yield was 4%. We know that dividends are more stable and reliable than stock prices, which is why dividends make ideal source of income in retirement. Dividends have only declined in a material way during the Great Depression of the 1929 – 1932. During the Great Recession of 2008 – 2009 dividends fell by 20%, which was nothing compared to the 50% declines in the broader market indexes. If capitalism is on its knees, only then do dividend payments suffer ( a third distant was the nationalization of equities from Russian investors in 1918).

Currently, popular US equity indices yield around 2%. It is possible to assemble a portfolio that yields 3% today if you are picky, but that is the best you can do today in the US in my opinion. Therefore, I do not believe that you can expect to “withdraw” 4% of your portfolio value under todays conditions. It may work if stock prices continue going up and you sell 2% of your holdings today, while generating the other 2% you need from dividends. Of course, if stock prices go nowhere, like they did between 1929 – 1954 or 1966 – 1982 or 2000 -2013, you may be in a little bit of a trouble if you have to sell stock for living expenses. Why would you be in trouble? Because you will increase your risk of running out of money in retirement.

There are a lot of academic models that discuss things like beta, alpha, covariance, optimal portfolios etc. However, I take these with a grain of salt as well. Academicians are great at torturing data, until they find something worthy of publishing in a journal. But their success in the world is not typically based on the performance of that model with real money. Smart people can be blinded by simple things, and may end up overcomplicating matters. For example, the geniuses at Long Term Capital Management had elaborate formulas to extract consistent profits for almost 4 years. However, they were overleveraged and their success depended on the the past being like the present. They failed, and inspired a nice book titled “When Geniuses Failed”. We are not geniuses, and our success in the real world is dependent on how our portfolios do, and how much reliable income they can produce to sustain us in retirement.

I believe that creating margins of safety, overlapping systems and different buffers can be great tools in the toolbox of the investor who wants to live off their nest egg in retirement. It is also important to have margin of safety in everything you do when in comes to investing. This means being diversified, making sure that there is an adequate payout ratio, that valuation is not overstretched and that no leverage is being used. It also means keeping investment costs low, sticking to your strategy through thick or thin and focusing on buy and hold investing.

This involves being diversified, buying blue chip companies at attractive valuations, buying over time. It may also involve generating income not just from dividends, but also from fixed income and pensions/social security. Owning your home outright may be another diversification tool, because you will need less income in retirement if you do not have a recurring rent or mortgage payment ( despite the fact that there is an opportunity cost in locking up your money in an illiquid asset that could be earning more elsewhere).

Going back to the point, I believe that it doesn’t make sense to have a list of great companies to buy at all times. The conditions to acquire companies vary from one period to the next. For example, my decision to buy 3M will be favorable if it is earning $10/share and selling for $150/share but unfavorable if it is earning $10/share but selling for $300/share.

In another example, I liked P&G (PG) until historical earnings per share were generally moving upwards. Due to the lack of earnings growth since 2008 however, it doesn’t make business sense to acquire ownership interests in this otherwise resilient business. In addition to that, it is selling at more than 20 times forward earnings. Therefore, it is a double-whammy. If P&G manages to resume earnings growth, and starts selling at 15 times earnings, I may consider it for investment again.

This is why as an investor, I try to buy stocks regularly, and picking the values I could find at the moment. If I do this for a long enough period of time, I would be able to buy securities from different sectors, by taking advantage of the sales being offered when different industries go in and out of style. This is a similar strategy to buying more when things are on sale at your local Wal-Mart and buying less of other items that have recently been marked up. It intuitively makes sense that as an investor in the accumulation phase, I am excited to see when stocks are down in price. This means that future retirement income is on sale.

Relevant Articles:

- Margin of Safety in Financial Independence

- Another reason for companies to pay dividends

- My Entry Criteria for Dividend Stocks

- Diversified Dividend Portfolios – Don’t forget about quality

Thursday, May 30, 2019

Tuesday, May 28, 2019

Eleven Dividend Growth Stocks In The News

It is time for my weekly review of notable dividend increases from the past week. This review is part of my monitoring process. It is also a good exercise showing investors how I quickly evaluate companies, before deciding to put them aside or place them on my list for further research. In this review, I look at the companies which hiked dividends last week.

I typically look for shareholder friendly companies which generate excess cashflows and share them with stockholders. Companies which have been able to increase dividends for at least ten consecutive years make very good first impression.

Companies with increasing earnings per share earn positive scores, because they show their past dividend growth was rooted in growth in fundamentals. Future growth in earnings will provide the launching pad for further dividend increases in the future.

I’m also looking for companies with safe dividends, which have adequate margins of safety, in order to lower the likelihood of dividend cuts during the next recession. An adequate payout ratio below 60%, coupled with a relative stability in earnings throughout past economic recessions is a good first start. Of course, growing earnings per share also provide an extra cushion to an adequate dividend payout ratio. A high payout ratio may be acceptable only in the cases where companies have maintained it for a long time or they have a business model or business structure (e.g. a REIT) which is usually associated with a high payout ratio.

Last but not least, I like to focus on valuation. I believe that even the best dividend paying company in the world is not worth overpaying for. A lower entry price can provide better long-term returns to investors on average.

As a result, there are several dividend growth stocks which met these criteria. The companies in this weeks review include:

Flowers Foods, Inc. (FLO) produces and markets bakery products in the United States. The company operates through two segments, Direct-Store-Delivery and Warehouse Delivery.

The company raised its quarterly dividend by 5.60% to 19 cents/share. This marked the 18th consecutive annual dividend increase for this dividend achiever. The latest dividend increase is slower than the ten-year average of 10.80%/year. The company’s dividend yield at the new quarterly rate is at 3.30%.

Between 2009 and 2018, the company grew its earnings from 63 cents/share to 74 cents/share. Flowers Foods is expected to generate $0.97/share in 2019.

The stock is overvalued at 23.70 times forward earnings. The rate of earnings growth also seems low.

Ashland Global Holdings Inc. (ASH) provides specialty chemical solutions worldwide.

The company raised its quarterly dividend by 10% to 27.50 cents/share, which was the tenth year of consecutive annual dividend increase for Ashland. This increase was faster than the company’s ten-year average of 8.30%/year. The company’s dividend yield at the new rate is 1.50%.

Between 2009 and 2018, the company grew its earnings from $0.96/share to $1.79/share. The company is expected to earn $3.03/share in 2019. Earnings per share are difficult to evaluate, due to spin-offs and assets being sold over the past decade in an effort to focus on specialty chemicals.

The stock is also overvalued at 24.30 times forward earnings.

First Financial Corporation (THFF), through its subsidiaries, provides various financial services.

The company raised its quarterly dividend by 2% to 52 cents/share. This was slower than the ten-year average increase of 1.50%/year. The company’s dividend yield at the new quarterly rate is 5.40% today. The latest increase marked the 31st consecutive annual dividend increase for this dividend champion.

Between 2009 and 2018, the company grew its earnings from $1.73/share to $3.80/share. The company is expected to generate $3.59/share in 2019.

The stock seems attractively valued at 10.80 times forward earnings. Given the slow rate of dividend growth, I believe that the stock may be more suitable for retirees looking for high current income, and may not worry if dividend income slowly loses purchasing power to inflation.

Lennox International Inc. (LII), provides climate control solutions in North America, Europe, Russia, Turkey, the Middle East, and internationally.

The company hiked its quarterly dividend by 20.30% to 77 cents/share. This marked the tenth consecutive annual dividend increase for this newly minted dividend contender. Over the past decade, Lennox has been able to hike its annual dividends at a rate of 15.20%/year. The dividend yield is at 1.10% at the new quarterly rate.

Between 2009 and 2018, the company managed to boost earnings per share from 90 cents/share to $8.74/share. Lennox International is expected to earn $12.33/share in 2019. Lennox looks like a quality company to acquire at the right price.

Unfortunately, the stock is overvalued today at 22.20 times forward earnings. It may be worth a second look if it dips below 20 times earnings.

Stock Yards Bancorp, Inc. (SYBT) operates as the holding company for Stock Yards Bank & Trust Company that provides commercial and personal banking services in Louisville, Indianapolis, and Cincinnati.

The bank increased its quarterly dividend by 4% to 26 cents/share. This marked the tenth consecutive year of dividend increases for this newly minted dividend contender. During the past decade, it managed to grow the dividend at an annual rate of 7.80%/year.

Between 2009 and 2018, the companies increased earnings from 79 cents/share to $2.42/share. The company is expected to generate $2.57/share in 2019. It is amazing to see earnings per share growing very nicely for almost 30 years, with the brief exception during the Global Financial Crisis. While dividends were kept unchanged during the crisis, this is far better than the widespread dividend cuts experienced by other financial institutions. This is a company to put on my list for further research.

The stock is attractively valued at 13.50 times forward earnings and yields 3%. I would add the stock to my list for further research.

Universal Corporation (UVV) engages in the supply of leaf tobacco products worldwide. The company operates through North America, South America, Africa, Europe, Asia, Dark Air-Cured, Oriental, and Special Services segments.

Universal hiked its quarterly dividend by 1.30% to 76 cents/share. This marked the 48th year of consecutive annual dividend increases for this dividend champion. During the past decade, the company has been able to grow dividends at an annual rate of 3.70%/year.

Universal’s earnings have been flat mostly, eking out a small gain from $4.03/share in 2008 to $4.11/share in 2018. This means that the company has also been largely unable to grow earnings per share since 1998.

Universal looks cheap at 14 times earnings. The stock yields 5.30% and has a payout ratio of 74%. Given the lack of earnings growth over the past 20 years, I believe that dividend growth has a natural limit to it. I believe that the dividend is probably safe for now, but I wouldn’t expect more than token dividend increases during the next 10 years. This security may be a decent fit for retirees who need current income today, and do not care if the purchasing power of that income may decrease over time.

V.F. Corporation (VFC) engages in the design, production, procurement, marketing, and distribution of branded lifestyle apparel, footwear, and related products for men, women, and children in the Americas, Europe, and the Asia Pacific. It operates through four segments: Outdoor & Action Sports, Jeanswear, Imagewear, and Other.

V.F. Corp increased its quarterly dividend by 6.25% to 51 cents/share. This marked the 47th year of annual dividend increases for this dividend champion. Over the past decade, it has managed to boost dividends at an annual rate of 12.50%.

Between 2009 and 2018, the company managed to boost earnings from $1.29/share to $3.15/share. V.F. Corp is expected to generate $3.76/share in 2019.

Unfortunately, the stock is overvalued today at 22.30 times forward earnings and yields 2.40%. V.F. Corp may be worth a second look if it is available below 20 times earnings.

The Clorox Company (CLX) manufactures and markets consumer and professional products worldwide. It operates through four segments: Cleaning, Household, Lifestyle, and International.

Clorox hiked its quarterly dividend by 10.40% to $1.06/share. This marked the 42nd consecutive annual dividend increase for this dividend champion. Clorox has managed to boost dividends at an annualized rate of 8% over the past decade. The dividend yield comes out to 2.80% today at the newly increased quarterly rate.

Between 2009 and 2018, Clorox managed to boost earnings from $3.79/share to $6.26/share. The company is expected to generate $6.28/share in 2019.

The stock is overvalued at 23.80 times forward earnings today. Clorox may be worth a look on dips below 20 times earnings.

Monro, Inc. (MNRO) provides automotive undercar repair, and tire sales and services in the United States.

The company hiked its quarterly dividend by 10% to 22 cents/share. This increase marked the 15th consecutive year of dividend hikes for this dividend achiever. During the past decade, it has managed to increase dividends at an annual rate of 17.20%/year. The stock yields 1.06% at the new dividend rate.

Monro has managed to grow earnings from $0.80/share in 2009 to $1.92/share in 2018. Monro is expected to generate $2.39/share in 2019.

The company’s stock is overvalued at 34.50 times forward earnings.

FactSet Research Systems Inc. (FDS) provides integrated financial information and analytical applications to the investment community in the United States, Europe, and the Asia Pacific.

The company increased its quarterly dividend by 12.50% to 72 cents/share. This marked the 21st year of annual dividend increases for this dividend achiever. Over the past decade, it has managed to grow distributions at an annualized rate of 14.20%/year. The dividend yield is low at 1% today, but this company can grow those distributions at a rate that can double them every five years.

Between 2009 and 2018, the company managed to boost its earnings from $2.97/share to $6.78/share. FactSet Research Systems is expected to earn $9.59/share in 2019.

The stock is overvalued at 29.20 times forward earnings. FactSet Research Systems may be worth a second look when it trades below 20 times earnings.

Extra Space Storage Inc. (EXR), headquartered in Salt Lake City, Utah, is a self-administered and self-managed REIT. The Company offers customers a wide selection of conveniently located and secure storage units across the country, including boat storage, RV storage and business storage.

The company raised its quarterly dividend by 4.70% to 90 cents/share. This raise is slower than the ten year average of 12.90%/year. The latest increase brings the streak of annual dividend increases to ten.

FFO/share increased from $1.18 in 2008 to $4.62 in 2018. This looks like a good growth during the past decade.

The REIT is selling at 23.10 times FFO, which seems a little high for a REIT. It yields almost 3.40% today. While I view the REIT as overvalued, it may be worth adding to the list for further research.

Relevant Articles:

- This is why we diversify

- How to determine if your dividends are safe

- 2019 Dividend Champions List

- How to avoid dividend cuts

I typically look for shareholder friendly companies which generate excess cashflows and share them with stockholders. Companies which have been able to increase dividends for at least ten consecutive years make very good first impression.

Companies with increasing earnings per share earn positive scores, because they show their past dividend growth was rooted in growth in fundamentals. Future growth in earnings will provide the launching pad for further dividend increases in the future.

I’m also looking for companies with safe dividends, which have adequate margins of safety, in order to lower the likelihood of dividend cuts during the next recession. An adequate payout ratio below 60%, coupled with a relative stability in earnings throughout past economic recessions is a good first start. Of course, growing earnings per share also provide an extra cushion to an adequate dividend payout ratio. A high payout ratio may be acceptable only in the cases where companies have maintained it for a long time or they have a business model or business structure (e.g. a REIT) which is usually associated with a high payout ratio.

Last but not least, I like to focus on valuation. I believe that even the best dividend paying company in the world is not worth overpaying for. A lower entry price can provide better long-term returns to investors on average.

As a result, there are several dividend growth stocks which met these criteria. The companies in this weeks review include:

Flowers Foods, Inc. (FLO) produces and markets bakery products in the United States. The company operates through two segments, Direct-Store-Delivery and Warehouse Delivery.

The company raised its quarterly dividend by 5.60% to 19 cents/share. This marked the 18th consecutive annual dividend increase for this dividend achiever. The latest dividend increase is slower than the ten-year average of 10.80%/year. The company’s dividend yield at the new quarterly rate is at 3.30%.

Between 2009 and 2018, the company grew its earnings from 63 cents/share to 74 cents/share. Flowers Foods is expected to generate $0.97/share in 2019.

The stock is overvalued at 23.70 times forward earnings. The rate of earnings growth also seems low.

Ashland Global Holdings Inc. (ASH) provides specialty chemical solutions worldwide.

The company raised its quarterly dividend by 10% to 27.50 cents/share, which was the tenth year of consecutive annual dividend increase for Ashland. This increase was faster than the company’s ten-year average of 8.30%/year. The company’s dividend yield at the new rate is 1.50%.

Between 2009 and 2018, the company grew its earnings from $0.96/share to $1.79/share. The company is expected to earn $3.03/share in 2019. Earnings per share are difficult to evaluate, due to spin-offs and assets being sold over the past decade in an effort to focus on specialty chemicals.

The stock is also overvalued at 24.30 times forward earnings.

First Financial Corporation (THFF), through its subsidiaries, provides various financial services.

The company raised its quarterly dividend by 2% to 52 cents/share. This was slower than the ten-year average increase of 1.50%/year. The company’s dividend yield at the new quarterly rate is 5.40% today. The latest increase marked the 31st consecutive annual dividend increase for this dividend champion.

Between 2009 and 2018, the company grew its earnings from $1.73/share to $3.80/share. The company is expected to generate $3.59/share in 2019.

The stock seems attractively valued at 10.80 times forward earnings. Given the slow rate of dividend growth, I believe that the stock may be more suitable for retirees looking for high current income, and may not worry if dividend income slowly loses purchasing power to inflation.

Lennox International Inc. (LII), provides climate control solutions in North America, Europe, Russia, Turkey, the Middle East, and internationally.

The company hiked its quarterly dividend by 20.30% to 77 cents/share. This marked the tenth consecutive annual dividend increase for this newly minted dividend contender. Over the past decade, Lennox has been able to hike its annual dividends at a rate of 15.20%/year. The dividend yield is at 1.10% at the new quarterly rate.

Between 2009 and 2018, the company managed to boost earnings per share from 90 cents/share to $8.74/share. Lennox International is expected to earn $12.33/share in 2019. Lennox looks like a quality company to acquire at the right price.

Unfortunately, the stock is overvalued today at 22.20 times forward earnings. It may be worth a second look if it dips below 20 times earnings.

Stock Yards Bancorp, Inc. (SYBT) operates as the holding company for Stock Yards Bank & Trust Company that provides commercial and personal banking services in Louisville, Indianapolis, and Cincinnati.

The bank increased its quarterly dividend by 4% to 26 cents/share. This marked the tenth consecutive year of dividend increases for this newly minted dividend contender. During the past decade, it managed to grow the dividend at an annual rate of 7.80%/year.

Between 2009 and 2018, the companies increased earnings from 79 cents/share to $2.42/share. The company is expected to generate $2.57/share in 2019. It is amazing to see earnings per share growing very nicely for almost 30 years, with the brief exception during the Global Financial Crisis. While dividends were kept unchanged during the crisis, this is far better than the widespread dividend cuts experienced by other financial institutions. This is a company to put on my list for further research.

The stock is attractively valued at 13.50 times forward earnings and yields 3%. I would add the stock to my list for further research.

Universal Corporation (UVV) engages in the supply of leaf tobacco products worldwide. The company operates through North America, South America, Africa, Europe, Asia, Dark Air-Cured, Oriental, and Special Services segments.

Universal hiked its quarterly dividend by 1.30% to 76 cents/share. This marked the 48th year of consecutive annual dividend increases for this dividend champion. During the past decade, the company has been able to grow dividends at an annual rate of 3.70%/year.

Universal’s earnings have been flat mostly, eking out a small gain from $4.03/share in 2008 to $4.11/share in 2018. This means that the company has also been largely unable to grow earnings per share since 1998.

Universal looks cheap at 14 times earnings. The stock yields 5.30% and has a payout ratio of 74%. Given the lack of earnings growth over the past 20 years, I believe that dividend growth has a natural limit to it. I believe that the dividend is probably safe for now, but I wouldn’t expect more than token dividend increases during the next 10 years. This security may be a decent fit for retirees who need current income today, and do not care if the purchasing power of that income may decrease over time.

V.F. Corporation (VFC) engages in the design, production, procurement, marketing, and distribution of branded lifestyle apparel, footwear, and related products for men, women, and children in the Americas, Europe, and the Asia Pacific. It operates through four segments: Outdoor & Action Sports, Jeanswear, Imagewear, and Other.

V.F. Corp increased its quarterly dividend by 6.25% to 51 cents/share. This marked the 47th year of annual dividend increases for this dividend champion. Over the past decade, it has managed to boost dividends at an annual rate of 12.50%.

Between 2009 and 2018, the company managed to boost earnings from $1.29/share to $3.15/share. V.F. Corp is expected to generate $3.76/share in 2019.

Unfortunately, the stock is overvalued today at 22.30 times forward earnings and yields 2.40%. V.F. Corp may be worth a second look if it is available below 20 times earnings.

The Clorox Company (CLX) manufactures and markets consumer and professional products worldwide. It operates through four segments: Cleaning, Household, Lifestyle, and International.

Clorox hiked its quarterly dividend by 10.40% to $1.06/share. This marked the 42nd consecutive annual dividend increase for this dividend champion. Clorox has managed to boost dividends at an annualized rate of 8% over the past decade. The dividend yield comes out to 2.80% today at the newly increased quarterly rate.

Between 2009 and 2018, Clorox managed to boost earnings from $3.79/share to $6.26/share. The company is expected to generate $6.28/share in 2019.

The stock is overvalued at 23.80 times forward earnings today. Clorox may be worth a look on dips below 20 times earnings.

Monro, Inc. (MNRO) provides automotive undercar repair, and tire sales and services in the United States.

The company hiked its quarterly dividend by 10% to 22 cents/share. This increase marked the 15th consecutive year of dividend hikes for this dividend achiever. During the past decade, it has managed to increase dividends at an annual rate of 17.20%/year. The stock yields 1.06% at the new dividend rate.

Monro has managed to grow earnings from $0.80/share in 2009 to $1.92/share in 2018. Monro is expected to generate $2.39/share in 2019.

The company’s stock is overvalued at 34.50 times forward earnings.

FactSet Research Systems Inc. (FDS) provides integrated financial information and analytical applications to the investment community in the United States, Europe, and the Asia Pacific.

The company increased its quarterly dividend by 12.50% to 72 cents/share. This marked the 21st year of annual dividend increases for this dividend achiever. Over the past decade, it has managed to grow distributions at an annualized rate of 14.20%/year. The dividend yield is low at 1% today, but this company can grow those distributions at a rate that can double them every five years.

Between 2009 and 2018, the company managed to boost its earnings from $2.97/share to $6.78/share. FactSet Research Systems is expected to earn $9.59/share in 2019.

The stock is overvalued at 29.20 times forward earnings. FactSet Research Systems may be worth a second look when it trades below 20 times earnings.

Extra Space Storage Inc. (EXR), headquartered in Salt Lake City, Utah, is a self-administered and self-managed REIT. The Company offers customers a wide selection of conveniently located and secure storage units across the country, including boat storage, RV storage and business storage.

The company raised its quarterly dividend by 4.70% to 90 cents/share. This raise is slower than the ten year average of 12.90%/year. The latest increase brings the streak of annual dividend increases to ten.

FFO/share increased from $1.18 in 2008 to $4.62 in 2018. This looks like a good growth during the past decade.

The REIT is selling at 23.10 times FFO, which seems a little high for a REIT. It yields almost 3.40% today. While I view the REIT as overvalued, it may be worth adding to the list for further research.

Relevant Articles:

- This is why we diversify

- How to determine if your dividends are safe

- 2019 Dividend Champions List

- How to avoid dividend cuts

Saturday, May 25, 2019

Dividend Growth Investor Newsletter Memorial Day Sale

Last year, I started a premium newsletter focusing on providing more actionable content for subscribers. I launched this service, particularly to address a common question I receive quite often from readers. Many readers ask either for a summary of my best ideas or for a listing of my dividend portfolio holdings.

One of the challenges I have is that I would not recommend purchasing many of the companies I own today due to valuation. However, I think that my newsletter addresses the need for a snapshot of dividend holdings for the long-term and a list of attractively valued companies that the portfolio will purchase each month.

In my newsletter, I run an actual dividend portfolio with real money. I invest every single month in the best values I can find at the moment. I allocate $1,000 per month to the portfolio. Each month, I try to invest in 10 blue chip dividend companies using the commission free brokerage Robinhood.

Each newsletter includes the ten companies I plan to buy for the Dividend Growth Portfolio. I try to provide more than just a list of companies I am buying however. You will be able to obtain an analysis of each company included in the portfolio through the newsletter. In my analysis, I will focus on dividend safety, dividend growth potential and valuation. I try to invest that money with utmost care, because I know that I will rely on that dividend income stream in the future. As the dividend portfolio matures, I will walk you through the process of managing portfolio weights, working on diversification and monitoring the portfolio.

The newsletter with ten dividend ideas comes out on the last Sunday of every month. The next newsletter comes out on May 26th. The orders will be executed at the open on Tuesday morning. Subscribers will receive confirmation about the purchases that are made in a follow up email later that day.

Each month, I also include a brief overview of the portfolio performance. The ultimate goal of this portfolio will be to generate $1,000 in safe monthly dividend income. Therefore, I have the commitment to stick to this portfolio for a few years.

Dividends are reinvested in the best values at the moment. They are pooled with the new cash deposits into the brokerage account. Once dividends earned in a given month reach $100 however, I may make investment decisions on an ad-hoc basis if I find a good value for the money that is short-lived. Subscribers will receive alerts for any real time trades made for the portfolio.

In order to thank you for being a loyal reader, I am offering the newsletter for a low introductory price of $76/year.

There is a 7 day free trial, during which your card will not be charged. After that, you can still cancel at any time, but you will be charged. For less than 20 cents/day, you will receive a listing of 10 quality companies that my real world portfolio will purchase every month. I believe that this is a bargain.

You can sign up below:

Once you subscribe, I will add you to my exclusive email list, and you will be able to receive premium information about the dividend growth investor portfolio.

You will receive the last newsletter from April 2019 upon signing up. The next newsletter will be sent out on May 26. I plan to provide an updated list of Dividend Portfolio Holdings by June 2.

The price will increase on June 1 to $79/year, so you have a limited chance to grab this limited time promotion today. If you subscribe today, your price will never increase. I guarantee it.

One of the challenges I have is that I would not recommend purchasing many of the companies I own today due to valuation. However, I think that my newsletter addresses the need for a snapshot of dividend holdings for the long-term and a list of attractively valued companies that the portfolio will purchase each month.

In my newsletter, I run an actual dividend portfolio with real money. I invest every single month in the best values I can find at the moment. I allocate $1,000 per month to the portfolio. Each month, I try to invest in 10 blue chip dividend companies using the commission free brokerage Robinhood.

Each newsletter includes the ten companies I plan to buy for the Dividend Growth Portfolio. I try to provide more than just a list of companies I am buying however. You will be able to obtain an analysis of each company included in the portfolio through the newsletter. In my analysis, I will focus on dividend safety, dividend growth potential and valuation. I try to invest that money with utmost care, because I know that I will rely on that dividend income stream in the future. As the dividend portfolio matures, I will walk you through the process of managing portfolio weights, working on diversification and monitoring the portfolio.

The newsletter with ten dividend ideas comes out on the last Sunday of every month. The next newsletter comes out on May 26th. The orders will be executed at the open on Tuesday morning. Subscribers will receive confirmation about the purchases that are made in a follow up email later that day.

Each month, I also include a brief overview of the portfolio performance. The ultimate goal of this portfolio will be to generate $1,000 in safe monthly dividend income. Therefore, I have the commitment to stick to this portfolio for a few years.

Dividends are reinvested in the best values at the moment. They are pooled with the new cash deposits into the brokerage account. Once dividends earned in a given month reach $100 however, I may make investment decisions on an ad-hoc basis if I find a good value for the money that is short-lived. Subscribers will receive alerts for any real time trades made for the portfolio.

In order to thank you for being a loyal reader, I am offering the newsletter for a low introductory price of $76/year.

There is a 7 day free trial, during which your card will not be charged. After that, you can still cancel at any time, but you will be charged. For less than 20 cents/day, you will receive a listing of 10 quality companies that my real world portfolio will purchase every month. I believe that this is a bargain.

You can sign up below:

Once you subscribe, I will add you to my exclusive email list, and you will be able to receive premium information about the dividend growth investor portfolio.

You will receive the last newsletter from April 2019 upon signing up. The next newsletter will be sent out on May 26. I plan to provide an updated list of Dividend Portfolio Holdings by June 2.

The price will increase on June 1 to $79/year, so you have a limited chance to grab this limited time promotion today. If you subscribe today, your price will never increase. I guarantee it.

Thursday, May 23, 2019

3M (MMM) Dividend Stock Analysis

3M Company (MMM) operates as a diversified technology company worldwide, which operates in five segments: Industrial, Safety and Graphics, Health Care, Electronics and Energy, and Consumer segments. This analysis was shared with subscribers to my Dividend Portfolio Newsletter earlier last week.

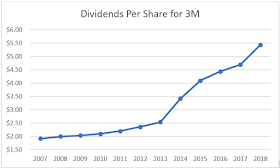

3M is a dividend king with a 61-year record of annual dividend increases. The company raised its quarterly dividend by 5.90% to $1.44/share in January 2019.

The company has managed to deliver a 4.30% average increase in annual EPS since 2007. 3M is expected to earn somewhere between $9.25 and $9.75/share in 2019. In comparison, the company earned $8.89/share in 2018.

The strength of 3M’s business model is largely driven by three key strategic levers: active portfolio management, investing in innovation, and business transformation. Management believes that these levers, combined with more aggressive capital deployment, will drive enhanced value creation. Over the last several years 3M has taken significant actions to strengthen its technology capabilities, improve portfolio and cost structure, and make the company even more relevant to customers. 3M’s technology platforms and its manufacturing scale allow it to achieve the lowest unit cost in most of the categories in which 3M competes. This also ensures high margins as well.

The first lever – Portfolio Management – is increasing customer relevance and allowing 3M to focus on its most profitable and fastest-growing businesses. 3M has realigned from 40 businesses to 24 over the past five years. This has resulted in SG&A savings of around $250 million. Continued portfolio management will also help to optimize its footprint, and the company is targeting $125 million to $175 million in additional operational savings by 2020. The company is also expecting that acquisitions, net of divestitures will result in a net 1% growth in annual sales over time. Portfolio management is strengthening 3M’s competitiveness and making them even more relevant to our customers and the marketplace.

Investing in Innovation is the second lever. 3M plans to increase investments in research and development to about 6 percent of sales. The company spends over 6% of revenues on R&D, and has been able to discover innovative products to bolster its bottom line. 3M also allows it engineers to spend 15% of their time on their own projects, which has resulted in a lot of innovation. The company has a proven track record of making money on its research dollars spent, as it tries to find applications with a customer centric point of view. The company invests in research and development to support organic growth, and enhance the company’s strong margins and return on invested capital.

3M continues to make good progress on its third lever – Business Transformation – which is enabling the company to better serve customers with even more agility and efficiency. Its Business Transformation lever aims to creating value for the company and its customers. By 2020, this initiative is expected to deliver $500 to $700 million in annual operational savings, and an additional $500 million reduction in working capital.

The company is also focusing on investments in priority growth platforms such as auto electrification, air quality and personal safety. The company is also focusing investments on its strong global business model including in the U.S. and China.

Recently, the stock has been battered, after it missed earnings and revenue projections. 3M cut EPS guidance to $9.25-$9.75 from $10.45-$10.90 previously. The company is also trying to cut costs by eliminating 2,000 positions, which could likely save almost a quarter of a billion per year. I am not going to extrapolate this bad quarter onto the future and would see further declines as an opportunity to add on further weakness.

Earnings per share have also been aided by share buybacks. The number of shares outstanding has decreased from 732 million in 2007 to 602 million by 2018.

The annual dividend payment has increased by 10.50% per year over the past decade, which is higher than the growth in EPS. Future rates of growth in dividends will be limited to the rate of growth in earnings per share.

For more than a century the strings of 3M business model has enabled the company to invest in the business while also returning cash to our shareholders. All of this has included a strong steady and rising dividend which is management sees as the hallmark of the enterprise.

In the past decade, the dividend payout ratio has increased from 34% in 2007 to 61% in 2018. I believe that 3M's dividend is safe. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently, 3M is fairly valued at 17.60 times forward earnings and has a current yield of 3.40%. This quality company may be worth a second look in the $185 - $195/share range and may be even more interesting to me if it further dips from there.

Relevant Articles:

- Dividend Kings List For 2019

- Dividends versus Share Buybacks/Stock repurchases

- What drives future investment returns?

- Twelve Companies Raising Dividends To Their Investors

3M is a dividend king with a 61-year record of annual dividend increases. The company raised its quarterly dividend by 5.90% to $1.44/share in January 2019.

The company has managed to deliver a 4.30% average increase in annual EPS since 2007. 3M is expected to earn somewhere between $9.25 and $9.75/share in 2019. In comparison, the company earned $8.89/share in 2018.

The strength of 3M’s business model is largely driven by three key strategic levers: active portfolio management, investing in innovation, and business transformation. Management believes that these levers, combined with more aggressive capital deployment, will drive enhanced value creation. Over the last several years 3M has taken significant actions to strengthen its technology capabilities, improve portfolio and cost structure, and make the company even more relevant to customers. 3M’s technology platforms and its manufacturing scale allow it to achieve the lowest unit cost in most of the categories in which 3M competes. This also ensures high margins as well.

The first lever – Portfolio Management – is increasing customer relevance and allowing 3M to focus on its most profitable and fastest-growing businesses. 3M has realigned from 40 businesses to 24 over the past five years. This has resulted in SG&A savings of around $250 million. Continued portfolio management will also help to optimize its footprint, and the company is targeting $125 million to $175 million in additional operational savings by 2020. The company is also expecting that acquisitions, net of divestitures will result in a net 1% growth in annual sales over time. Portfolio management is strengthening 3M’s competitiveness and making them even more relevant to our customers and the marketplace.

Investing in Innovation is the second lever. 3M plans to increase investments in research and development to about 6 percent of sales. The company spends over 6% of revenues on R&D, and has been able to discover innovative products to bolster its bottom line. 3M also allows it engineers to spend 15% of their time on their own projects, which has resulted in a lot of innovation. The company has a proven track record of making money on its research dollars spent, as it tries to find applications with a customer centric point of view. The company invests in research and development to support organic growth, and enhance the company’s strong margins and return on invested capital.

3M continues to make good progress on its third lever – Business Transformation – which is enabling the company to better serve customers with even more agility and efficiency. Its Business Transformation lever aims to creating value for the company and its customers. By 2020, this initiative is expected to deliver $500 to $700 million in annual operational savings, and an additional $500 million reduction in working capital.

The company is also focusing on investments in priority growth platforms such as auto electrification, air quality and personal safety. The company is also focusing investments on its strong global business model including in the U.S. and China.

Recently, the stock has been battered, after it missed earnings and revenue projections. 3M cut EPS guidance to $9.25-$9.75 from $10.45-$10.90 previously. The company is also trying to cut costs by eliminating 2,000 positions, which could likely save almost a quarter of a billion per year. I am not going to extrapolate this bad quarter onto the future and would see further declines as an opportunity to add on further weakness.

Earnings per share have also been aided by share buybacks. The number of shares outstanding has decreased from 732 million in 2007 to 602 million by 2018.

The annual dividend payment has increased by 10.50% per year over the past decade, which is higher than the growth in EPS. Future rates of growth in dividends will be limited to the rate of growth in earnings per share.

For more than a century the strings of 3M business model has enabled the company to invest in the business while also returning cash to our shareholders. All of this has included a strong steady and rising dividend which is management sees as the hallmark of the enterprise.

In the past decade, the dividend payout ratio has increased from 34% in 2007 to 61% in 2018. I believe that 3M's dividend is safe. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently, 3M is fairly valued at 17.60 times forward earnings and has a current yield of 3.40%. This quality company may be worth a second look in the $185 - $195/share range and may be even more interesting to me if it further dips from there.

Relevant Articles:

- Dividend Kings List For 2019

- Dividends versus Share Buybacks/Stock repurchases

- What drives future investment returns?

- Twelve Companies Raising Dividends To Their Investors

Monday, May 20, 2019

Five Dividend Stocks Rewarding Shareholders With Raises

Last week, there were five dividend growth companies which increased distributions to their shareholders. Each of these companies has managed to grow distributions for at least ten consecutive years. I reviewed the most recent increase in dividends relative to the historical average. I also reviewed trends in earnings per share, in order to determine the likelihood of future dividend increases. In addition, I also reviewed valuation, in order to determine if a company is worth pursuing today, or it may be a better deal at a better price. I follow this process weekly, in an effort to monitor companies I own and to uncover potential opportunities for further research.

The companies for this weeks review include:

Marsh & McLennan Companies, Inc. (MMC), is a professional services company that provides advice and solutions to clients in the areas of risk, strategy, and people worldwide. It operates in two segments, Risk and Insurance Services, and Consulting.

The company increased its quarterly dividend by 9.60% to 46 cents/share. This marked the 10th consecutive year of annual dividend increases for this newly minted dividend contender. Marsh & McLennan has managed to grow dividends at an annualized rate of 7% over the past decade.

Between 2009 and 2018, the company managed to grow earnings from 42 cents/share to $3.23/share. Marsh & McLennan is expected to generate $4.60/share in 2019. The stock is a little overvalued at 20.80 times forward earnings and yields 1.90%. If valuation becomes more attractive, the stock may be worth a second look.

National Bankshares Inc. (NKSH) operates as the bank holding company for the National Bank of Blacksburg that provides retail and commercial banking services to individuals, businesses, non-profits, and local governments.

The company raised its semi-annual dividend by 6.40% to 67 cents/share. This marked the 20th year of annual dividend increases for this dividend achiever. During the past decade, it managed to grow these distributions at an annualized rate of 4.20%.

Earnings per share didn’t grow by much between 2009 and 2018, rising only from $2.06/share to $2.32/share. The bank is expected to generate $2.63/share in 2019.

National Bankshares is fairly valued at 15.70 times forward earnings and offers a dividend yield of 3.20%. Given the slow earnings growth, I may place this on the back burner for now.

Northrop Grumman Corporation (NOC), a security company, provides products in the areas of autonomous systems, cyber, space, strikes, and logistics and modernizations in the United States, the Asia Pacific, and internationally. The company operates through four segments: Aerospace Systems, Innovation Systems, Mission Systems, and Technology Services.

The company raised its quarterly dividend by 10% to $1.32/share. This marked the 16th consecutive annual dividend increase for this dividend achiever. During the past decade, it managed to grow distributions at an annual rate of 12.70%/year.

Between 2009 and 2018 earnings increased from $5.21/share to $18.49/share. Northrop Grumman is expected to generate earnings of $19.38/share in 2019.

Currently, the stock is fairly valued at 15.80 times forward earnings and offers a safe yield of 1.70%.

IDEX Corporation (IEX), through its subsidiaries, operates as an applied solutions company worldwide. The company operates through three segments: Fluid & Metering Technologies (FMT), Health & Science Technologies (HST), and Fire & Safety/Diversified Products (FSDP).

The company increased its quarterly dividend by 16.30% to 50 cents/share. This marked the tenth consecutive annual dividend increase for this newly minted dividend contender. During the past decade, it has managed to grow dividends at an annual rate of 13.20%/year.

Between 2009 and 2018, earnings rose from $1.40/share to $5.29/share. The company is expected to generate $5.82/share in 2019.

Unfortunately, this company is overvalued at 25.90 times forward earnings. The stock yields 1.30% today. It may be worth a second look if it dips below 20 times forward earnings, which is equivalent to decline below $116/share.

Marriott International, Inc. (MAR) operates, franchises, and licenses hotel, residential, and timeshare properties worldwide. The company operates through North American Full-Service, North American Limited-Service, and Asia Pacific segments. The company raised its quarterly dividend by 17.10% to 48 cents/share. This was in line with the ten year average increase of 17.30%/year. Marriott International managed to grow earnings from $0.96/share in 2008 to $5.38/share 2018. The company is expected to generate $6.10/share in 2019.

The stock is overvalued at 21.50 times forward earnings. It yields 1.50%. The hospitality industry has had a strong decade, which has resulted in growing earnings per share. The next recession will decrease earnings per share, and shrink multiples to a more reasonable level.

Relevant Articles:

- How to read my weekly dividend increase reports

- Dividend Investors Should Ignore Market Fluctuations

- Rising Earnings – The Source of Future Dividend Growth

- How to read my stock analysis reports

The companies for this weeks review include:

Marsh & McLennan Companies, Inc. (MMC), is a professional services company that provides advice and solutions to clients in the areas of risk, strategy, and people worldwide. It operates in two segments, Risk and Insurance Services, and Consulting.

The company increased its quarterly dividend by 9.60% to 46 cents/share. This marked the 10th consecutive year of annual dividend increases for this newly minted dividend contender. Marsh & McLennan has managed to grow dividends at an annualized rate of 7% over the past decade.

Between 2009 and 2018, the company managed to grow earnings from 42 cents/share to $3.23/share. Marsh & McLennan is expected to generate $4.60/share in 2019. The stock is a little overvalued at 20.80 times forward earnings and yields 1.90%. If valuation becomes more attractive, the stock may be worth a second look.

National Bankshares Inc. (NKSH) operates as the bank holding company for the National Bank of Blacksburg that provides retail and commercial banking services to individuals, businesses, non-profits, and local governments.

The company raised its semi-annual dividend by 6.40% to 67 cents/share. This marked the 20th year of annual dividend increases for this dividend achiever. During the past decade, it managed to grow these distributions at an annualized rate of 4.20%.

Earnings per share didn’t grow by much between 2009 and 2018, rising only from $2.06/share to $2.32/share. The bank is expected to generate $2.63/share in 2019.

National Bankshares is fairly valued at 15.70 times forward earnings and offers a dividend yield of 3.20%. Given the slow earnings growth, I may place this on the back burner for now.

Northrop Grumman Corporation (NOC), a security company, provides products in the areas of autonomous systems, cyber, space, strikes, and logistics and modernizations in the United States, the Asia Pacific, and internationally. The company operates through four segments: Aerospace Systems, Innovation Systems, Mission Systems, and Technology Services.

The company raised its quarterly dividend by 10% to $1.32/share. This marked the 16th consecutive annual dividend increase for this dividend achiever. During the past decade, it managed to grow distributions at an annual rate of 12.70%/year.

Between 2009 and 2018 earnings increased from $5.21/share to $18.49/share. Northrop Grumman is expected to generate earnings of $19.38/share in 2019.

Currently, the stock is fairly valued at 15.80 times forward earnings and offers a safe yield of 1.70%.

IDEX Corporation (IEX), through its subsidiaries, operates as an applied solutions company worldwide. The company operates through three segments: Fluid & Metering Technologies (FMT), Health & Science Technologies (HST), and Fire & Safety/Diversified Products (FSDP).

The company increased its quarterly dividend by 16.30% to 50 cents/share. This marked the tenth consecutive annual dividend increase for this newly minted dividend contender. During the past decade, it has managed to grow dividends at an annual rate of 13.20%/year.

Between 2009 and 2018, earnings rose from $1.40/share to $5.29/share. The company is expected to generate $5.82/share in 2019.

Unfortunately, this company is overvalued at 25.90 times forward earnings. The stock yields 1.30% today. It may be worth a second look if it dips below 20 times forward earnings, which is equivalent to decline below $116/share.

Marriott International, Inc. (MAR) operates, franchises, and licenses hotel, residential, and timeshare properties worldwide. The company operates through North American Full-Service, North American Limited-Service, and Asia Pacific segments. The company raised its quarterly dividend by 17.10% to 48 cents/share. This was in line with the ten year average increase of 17.30%/year. Marriott International managed to grow earnings from $0.96/share in 2008 to $5.38/share 2018. The company is expected to generate $6.10/share in 2019.

The stock is overvalued at 21.50 times forward earnings. It yields 1.50%. The hospitality industry has had a strong decade, which has resulted in growing earnings per share. The next recession will decrease earnings per share, and shrink multiples to a more reasonable level.

Relevant Articles:

- How to read my weekly dividend increase reports

- Dividend Investors Should Ignore Market Fluctuations

- Rising Earnings – The Source of Future Dividend Growth

- How to read my stock analysis reports

Thursday, May 16, 2019

Vodafone Cuts Dividends to Shareholders

On Tuesday of this week, British Company Vodafone (VOD) cut its dividend by 40%. Not surprisingly, this dividend cut occurred several months after its Chief Financial Officer had stated that the dividend will not be cut. The dividend is cut due to several factors such as the need for cash to invest in 5G, and to acquire Liberty Global’s operations in Germany, the Czech Republic, Hungary and Romania

Vodafone (VOD) had been an international dividend achiever, with an almost 30-year history of annual dividend increases. The last five years saw dividend growth slow down to 2%/year. This was a decrease from the 7% annual growth in the preceding five years.

I own a few shares of Vodafone, because of investments I made in 2013. Because of the low amount of shares I own, it would not be cost effective to sell. If I owned a more material amount of shares however, valued around $1000 or more, I would likely sell and reinvest the proceeds elsewhere. Verizon may be a decent option.

You may enjoy the dividend stock analysis of Vodafone from the time I was considering the investment.

The major reason I invested in Vodafone was because of the value opportunity at play. Vodafone distributed shares of Verizon it had acquired as a result of the sale of its stake in Verizon Wireless to the parent company. What was a value play initially, turned out to be a slightly longer term investment.

I have not been a big fan of telecom companies in general throughout the years. This has somewhat been influenced by the fact that I have spent quite a few years working in the sector. This means that it made little sense to also load up my portfolio with telecom stocks. I have not been very enthusiastic about the sector in general too, but I have had exposure to it through my investment in Verizon (VZ), Vodafone and even AT&T (T) from time to time ( I used to follow an options strategy, which I stopped due to hassle factor, despite consistent profitability). I also view technological changes as a negative for the telecom sector.

However, I had sold most of my Vodafone shares throughout the years, for one reason or another. The main reason is the fact that I consolidated a lot of my retirement plans, and ended up buying funds with the proceeds. I ultimately kept only a small position from a legacy retirement account.

I thought of walking you through my history with this company. I like to discuss and share my mistakes, because I view them as learning opportunities. I believe that embracing mistakes and learning from them is ultimately what separates the people who are able to succeed in long-term investing from those who do not stick with it.

It turns out that I invested $200 in Vodafone on October 7, 2013. I used Sharebuilder – I believe that I paid $1/investment back then, but for some reason the broker states that it was a free trade. I ended up buying 5.70 shares of the telecom giant.

After a dividend reinvestment, I received shares of Verizon, which were spun off from Vodafone, or 1.5227 to be exact. Following this distribution, Vodafone enacted a 6:11 reverse split in its shares. The reverse split reduced the number of Vodafone shares from 5.79 to 3.16. I then kept reinvesting Verizon and Vodafone distributions until 2018. This was the time when Etrade decided to buy the brokerage business of Sharebuilder (now Capital One). As a result, there was a time when dividends were received in cash and fractional shares had to be sold before the transition.

I had 3.88 shares of Vodafone at the time, which meant I ended up selling 0.88 shares at $24.22/share or a total of $21.31. I also received a dividend of $4.56 in August 2018, prior to the remaining 3 shares being sent to Etrade. After February’s dividend I am left with 3.0898 shares, with a grand total value of $49.62 as of 5/15/2019.

I had 1.85 shares of Verizon, which meant I ended up selling 0.85 shares at $51.59/share for a total of 43.85. I also received $1.69 in dividends until the one share of Verizon was transferred out to Etrade. After May’s dividend I am left with 1.02161 shares worth a grand total of $58.04.

Overall, that $200 investment from October 2013 is now worth a whopping $179.07. If Sharebuilder hadn’t moved the assets over to Etrade and I didn’t have to sell fractional shares or receive dividends in cash, I would assume I would have still had a small loss on this investment. The largest point is that from an opportunity cost of view, I missed out on gain in some of the US Dividend Champions or Aristocrats over these five years. I did learn (or reiterate in a way) a few lessons on my portfolio building and strategy process.

Some random reader might laugh at these comically low dollar amounts I am discussing here. It makes it seem like my portfolio is an amateurish endeavor. Yet, they would be missing the forest for the trees with this comment. I am discussing low dollar amounts, because I ended up owning only a small amount in the company relative to total portfolio size. I bought a stock where I was ultimately wrong. I minimized the impact of the error by having a very small amount invested in the future dividend cutter Vodafone. When I build a position, I scale in slowly. If the story changes, or I lose confidence in management or there are better opportunities, I divert my capital elsewhere. This is how I end up with a lot of small holdings, which is a great way to monitor investments.

I think that the lesson for me is to invest small amounts regularly in a collection of dividend paying stocks, which meet my criteria. This way, I am able to diversify my exposure and not be exposed to the fortunes or lack thereof of a single company. In addition, by investing regularly, I am building my position slowly and over time. As a result, I am able to view negative changes and deteriorating conditions as I go through my leisurely accumulation of the position. As I view these conditions, and I see that the stock no longer meets my entry criteria, I stop accumulating. This is why I have so many small positions scattered around – they looked good at a time, but due to changes in the environment, I stopped adding to them. Therefore, I limited that amount of capital at risk. I rarely sell, which is a good thing, because on the flip side, I never know which of my investments will be my best one.

On the other hand, building positions slowly also exposes me to the risk that I identify a great company, but by the time I am able to accumulate the target position amount the stock price is too overvalued. As a result, I am stuck with a small position relative to what I would want it to be.

I also tend to accumulate dividends in cash, and pool them together with new cash deposited into my brokerage account, in order to make investments in the best values at the moment. This further helps me to diversify investments per sector, geography and over time. If I had simply let dividends accumulate in cash from Vodafone and Verizon, I would have been left with 3.10 Vodafone shares worth $49.80 and 1.50 shares of Verizon worth $85.20. I would have received $27.07 in cash dividends from Vodafone and $17.20 in cash dividends from Verizon for a total of $179.30. This is very close to what my investments ended being worth after all as well. But in reality, the change is that these funds would have been invested elsewhere and hopefully compounded at a better rate that Vodafone.

So to summarize:

• Keep investing mistakes small

• Spread risk by diversifying in many companies and over time

• Stop investing when story changes

• Keep Spin-offs

• Use dividends elsewhere by reinvesting them selectively in best values of the moment

• Review investing mistakes regularly, in order to learn from them and become a better investor

Relevant Articles:

- Should I invest in AT&T and Verizon for high dividend income?

- Are these high yield dividends sustainable?

- Maintaining Moats in times of Technological Changes

- Nine Dividend Paying Stocks I Accumulated in the Past Month

Vodafone (VOD) had been an international dividend achiever, with an almost 30-year history of annual dividend increases. The last five years saw dividend growth slow down to 2%/year. This was a decrease from the 7% annual growth in the preceding five years.

I own a few shares of Vodafone, because of investments I made in 2013. Because of the low amount of shares I own, it would not be cost effective to sell. If I owned a more material amount of shares however, valued around $1000 or more, I would likely sell and reinvest the proceeds elsewhere. Verizon may be a decent option.

You may enjoy the dividend stock analysis of Vodafone from the time I was considering the investment.

The major reason I invested in Vodafone was because of the value opportunity at play. Vodafone distributed shares of Verizon it had acquired as a result of the sale of its stake in Verizon Wireless to the parent company. What was a value play initially, turned out to be a slightly longer term investment.

I have not been a big fan of telecom companies in general throughout the years. This has somewhat been influenced by the fact that I have spent quite a few years working in the sector. This means that it made little sense to also load up my portfolio with telecom stocks. I have not been very enthusiastic about the sector in general too, but I have had exposure to it through my investment in Verizon (VZ), Vodafone and even AT&T (T) from time to time ( I used to follow an options strategy, which I stopped due to hassle factor, despite consistent profitability). I also view technological changes as a negative for the telecom sector.

However, I had sold most of my Vodafone shares throughout the years, for one reason or another. The main reason is the fact that I consolidated a lot of my retirement plans, and ended up buying funds with the proceeds. I ultimately kept only a small position from a legacy retirement account.

I thought of walking you through my history with this company. I like to discuss and share my mistakes, because I view them as learning opportunities. I believe that embracing mistakes and learning from them is ultimately what separates the people who are able to succeed in long-term investing from those who do not stick with it.

It turns out that I invested $200 in Vodafone on October 7, 2013. I used Sharebuilder – I believe that I paid $1/investment back then, but for some reason the broker states that it was a free trade. I ended up buying 5.70 shares of the telecom giant.

After a dividend reinvestment, I received shares of Verizon, which were spun off from Vodafone, or 1.5227 to be exact. Following this distribution, Vodafone enacted a 6:11 reverse split in its shares. The reverse split reduced the number of Vodafone shares from 5.79 to 3.16. I then kept reinvesting Verizon and Vodafone distributions until 2018. This was the time when Etrade decided to buy the brokerage business of Sharebuilder (now Capital One). As a result, there was a time when dividends were received in cash and fractional shares had to be sold before the transition.

I had 3.88 shares of Vodafone at the time, which meant I ended up selling 0.88 shares at $24.22/share or a total of $21.31. I also received a dividend of $4.56 in August 2018, prior to the remaining 3 shares being sent to Etrade. After February’s dividend I am left with 3.0898 shares, with a grand total value of $49.62 as of 5/15/2019.

I had 1.85 shares of Verizon, which meant I ended up selling 0.85 shares at $51.59/share for a total of 43.85. I also received $1.69 in dividends until the one share of Verizon was transferred out to Etrade. After May’s dividend I am left with 1.02161 shares worth a grand total of $58.04.

Overall, that $200 investment from October 2013 is now worth a whopping $179.07. If Sharebuilder hadn’t moved the assets over to Etrade and I didn’t have to sell fractional shares or receive dividends in cash, I would assume I would have still had a small loss on this investment. The largest point is that from an opportunity cost of view, I missed out on gain in some of the US Dividend Champions or Aristocrats over these five years. I did learn (or reiterate in a way) a few lessons on my portfolio building and strategy process.

Some random reader might laugh at these comically low dollar amounts I am discussing here. It makes it seem like my portfolio is an amateurish endeavor. Yet, they would be missing the forest for the trees with this comment. I am discussing low dollar amounts, because I ended up owning only a small amount in the company relative to total portfolio size. I bought a stock where I was ultimately wrong. I minimized the impact of the error by having a very small amount invested in the future dividend cutter Vodafone. When I build a position, I scale in slowly. If the story changes, or I lose confidence in management or there are better opportunities, I divert my capital elsewhere. This is how I end up with a lot of small holdings, which is a great way to monitor investments.

I think that the lesson for me is to invest small amounts regularly in a collection of dividend paying stocks, which meet my criteria. This way, I am able to diversify my exposure and not be exposed to the fortunes or lack thereof of a single company. In addition, by investing regularly, I am building my position slowly and over time. As a result, I am able to view negative changes and deteriorating conditions as I go through my leisurely accumulation of the position. As I view these conditions, and I see that the stock no longer meets my entry criteria, I stop accumulating. This is why I have so many small positions scattered around – they looked good at a time, but due to changes in the environment, I stopped adding to them. Therefore, I limited that amount of capital at risk. I rarely sell, which is a good thing, because on the flip side, I never know which of my investments will be my best one.

On the other hand, building positions slowly also exposes me to the risk that I identify a great company, but by the time I am able to accumulate the target position amount the stock price is too overvalued. As a result, I am stuck with a small position relative to what I would want it to be.

I also tend to accumulate dividends in cash, and pool them together with new cash deposited into my brokerage account, in order to make investments in the best values at the moment. This further helps me to diversify investments per sector, geography and over time. If I had simply let dividends accumulate in cash from Vodafone and Verizon, I would have been left with 3.10 Vodafone shares worth $49.80 and 1.50 shares of Verizon worth $85.20. I would have received $27.07 in cash dividends from Vodafone and $17.20 in cash dividends from Verizon for a total of $179.30. This is very close to what my investments ended being worth after all as well. But in reality, the change is that these funds would have been invested elsewhere and hopefully compounded at a better rate that Vodafone.

So to summarize:

• Keep investing mistakes small

• Spread risk by diversifying in many companies and over time

• Stop investing when story changes

• Keep Spin-offs

• Use dividends elsewhere by reinvesting them selectively in best values of the moment

• Review investing mistakes regularly, in order to learn from them and become a better investor

Relevant Articles:

- Should I invest in AT&T and Verizon for high dividend income?

- Are these high yield dividends sustainable?

- Maintaining Moats in times of Technological Changes

- Nine Dividend Paying Stocks I Accumulated in the Past Month

Monday, May 13, 2019

Ten Dividend Stocks Providing Consistent Raises to Shareholders

As part of my monitoring process, I look at the list of dividend increases every week. I usually focus my attention on the companies that have managed to grow dividends for at least a decade. As a result, I didn’t include shares of Tractor Supply (TSCO), which is a company whose story I am monitoring.

I also tend to focus on the companies that are growing dividends by more than a token amount, unless of course I own them. As a result, I didn’t include shares of Microchip Technologies (MCHP), which is raising distributions at a slow rate of less than 1%/year.

For the companies that are left to review, I look at the dividend increase relative to the ten-year average, to determine if dividend increases are moving in the right direction.

I also review the growth in earnings per share and payout ratio, in order to determine if the dividend is safe, and if there is room for further dividend increases down the road.

Last but not least, I also review valuation per my valuation guidelines. Even the best dividend growth stock in the world is not worth buying at excessively high valuation levels.

These are very similar to the criteria I use in my dividend stock analyses. The ideas I use to review companies are also the same types of attributes I use to put companies on the list for further research, to hold off until the right price or to quickly discard into the ‘too hard” box.

One of the reasons why I share these lists is to illustrate my criteria in action, hope to educate others about tools they could implement into their own process. Speaking of process, I find it very important to develop your own process, and to follow it, by continuously improving it as well.

Over the past week, there were several companies that increased dividends. Aside from the ones I already mentioned in a previous post, the companies in todays review include:

Chesapeake Utilities Corporation (CPK), a diversified energy company, engages in regulated and unregulated energy businesses. The company operates in two segments, Regulated Energy and Unregulated Energy.

The company hiked its quarterly dividend by 9.50% to 40.50 cents/share. This marked the 16th consecutive annual dividend increase for this dividend achiever. During the past decade, this company has been able to grow distributions at an annual rate of 5.70%.

Chesapeake Utilities managed to boost earnings from $1.43/share in 2009 to $3.45/share in 2018. Chesapeake Utilities is expected to earn $3.70/share in 2019.

The stock is overvalued at 25.70 times forward earnings and yields 1.70%.

Expeditors International of Washington, Inc. (EXPD) provides logistics services in the Americas, North Asia, South Asia, Europe, the Middle East, Africa, and India.

The company hiked its semi-annual dividend by 11.10% to 50 cents/share. This marked the 25th consecutive annual dividend increase for this newly minted dividend champion. The latest dividend hike is in line with the ten year average of 10.90%/year.

Between 2009 and 2018, Expeditors International managed to boost earnings from $1.11/share to $3.48/share. Expeditors International is expected to earn $3.55/share in 2019.

The stock is slightly overvalued at 20.80 times forward earnings and yields 2.70%. I will consider reviewing the stock if it drops below $71/share.

MSA Safety Incorporated (MSA) develops, manufactures, and supplies safety products that protect people and facility infrastructures in the oil, gas, petrochemical, fire service, construction, utilities, and mining industries worldwide. It operates through Americas and International segments.

The company approved a 10.50% increase in its quarterly dividend to 42 cents/share. This marked the 48th year of annual dividend increases for this dividend champion. During the past decade, it has managed to grow the annual dividends at a rate of 4.70%/year.

The company managed to grow earnings from $1.21/share in 2009 to $3.18/share in 2018.

MSA Safety is expected to earn $4.82/share in 2019. The stock is overvalued at 22.50 times forward earnings and yields 1.55%.

NACCO Industries, Inc. (NC), operates surface mines that supply bituminous coal and lignite primarily to power generation companies.

The company hiked its quarterly dividend by 15.20% to 19 cents/share. This marked the 34th year of annual dividend increase for this dividend champion. During the past decade, it managed to grow its dividends at a rate of 12.40%/year. From a fundamentals perspective, NACCO is more challenging to analyze, because the company from a decade ago is different from the company today due to two large spin-offs in 2012 and 2017. NACCO earned $5/share in 2018, which was higher than the $4.41/share it earned in 2017 – the first year as a stand-alone company.