A few years ago when I started my site I made a prediction that dividends might become the next big bubble in the making. After two stock market crashes, record low interest rates and the increase in the number of individuals who rely exclusively on their nest eggs for retirement, investors were bound to start chasing dividend stocks.

Over the past several months, I have read several articles discussing whether we are in a dividend stock bubble or not. Back in early January I mentioned that I did not believe we are in a bubble. I decided to join the conversation again, and provide my audience with a balanced outlook on things. I define a dividend bubble as a situation where investor expectations have pushed valuations beyond overvalued territory.

Some pockets in the market are indeed in a dividend bubble. High yield stocks such as utilities and REITs are trading at 52 week highs. Their yields are at multi-year lows. The problem with these stocks is that many tend to raise dividends at a very slow pace, because their earnings power does not increase by much over time. Due to the low interest rates, investors have simply chased these yield stocks which has led to decreases in yield. If inflation were to pick up, investors in utilities would be beaten up on three fronts – low initial yields, low dividend growth that fails to compensate for inflation and earnings which would suffer if inflation pushes interest rates back up.

For example, companies like Con Edison (ED), which have been raising distributions by 1% /year for the past 15 years are yielding less than 4% today. Given the low earnings growth, high payout ratios and lowest yield in decades, investors in this New York based utility might be in for a rude awakening a few years from now.

Other companies such as Coca-Cola (KO) are trading at 20 times earnings. This is also overvalued territory, and investors who purchase stocks at high multiples are taking on a lot of unnecessary risk. Even the best dividend growth stocks in the world are not worth owning at any price. In fact, one of the main reasons behind the lackluster performance of US stocks since 2000 is the fact that they were grossly overvalued at the beginning of the millennium. Even such dividend growth stars as Coca-Cola (KO) and Johnson & Johnson (JNJ) traded at absurd multiples. As a result, while earnings and dividends grew over the next decade, stock prices of these quality companies remained flat until they got into buy territory just recently.

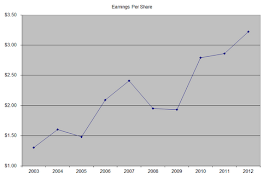

There are also some companies that “look overvalued” to the naked eye. Companies like Johnson & Johnson (JNJ) appear to be trading at P/E ratios above 20. Dividend investors should focus on recurring earnings, while ignoring one-time charge-offs that do not affect recurring earnings. For example, back in the fourth quarter of 2011, Johnson & Johnson (JNJ) earned only 8 cents/share. Adding the earnings for the next three quarters totals $3.04/share. At current prices, this equates to a P/E of 23.30. If one takes the time to read the 4th quarter earnings release, they could see the following:

Fourth-quarter 2011 net earnings reflect after-tax charges of $2.9 billion, which include product liability expenses, the net impact of litigation settlements, costs associated with the DePuy ASR™ Hip recall program, and an adjustment to the value of a currency option and costs related to the planned acquisition of Synthes, Inc. Fourth-quarter 2010 net earnings included after-tax charges of $922 million representing product liability expenses, the net impact of litigation settlements, and costs associated with the DePuy ASR™ Hip recall program. Excluding these special items for both periods, net earnings for the current quarter were $3.1 billion and diluted earnings per share were $1.13, representing increases of 9.3% and 9.7%, respectively, as compared to the same period in 2010.

Adding back the $1.05/share, and EPS comes out to $4.09/share. But there was another one-time charge that JNJ recorded in Q2 2012:

Second-quarter 2012 net earnings include after-tax special items of $2.2 billion, consisting of non-cash charges primarily attributed to a partial write-down of in-process research and development and intangible assets related to the Crucell vaccines business, an increase in the accrual for the potential settlement of previously disclosed civil litigation matters, and transaction and integration costs related to the acquisition of Synthes, Inc. Second-quarter 2011 net earnings included after-tax special items of $772 million, consisting of net charges related to the restructuring by Cordis Corporation, the net impact of expenses related to litigation, DePuy ASR™ Hip recall costs, and a currency adjustment related to the acquisition of Synthes, Inc. Excluding these special items, net earnings for the current quarter were $3.6 billion and diluted earnings per share were $1.30, representing increases of 2.7% and 1.6%, respectively, as compared to the same period in 2011.

Without these one-time deals, earnings per share for Johnson & Johnson (JNJ) would have been 4.89/share, which makes current P/E ratio to be 14.50.

In general however, dividend investing continues to be a stock pickers market. Investors who harvest the fruit of their income portfolios tend to spend some time screening the market for quality stocks at bargain prices, according to their predefined entry criteria. I still find companies trading at P/E ratios of less than 15 times earnings:

Aflac Incorporated (AFL), through its subsidiary, American Family Life Assurance Company of Columbus, provides supplemental health and life insurance. The company has raised dividends for 30 years in a row. Over the past decade, this dividend champion has managed to boost distributions by 20.40% per year. Aflac currently trades at 8.10 times earnings and yields 2.80%. (analysis)

Chevron Corporation, through its subsidiaries, engages in petroleum, chemicals, mining, power generation, and energy operations worldwide. The company has raised dividends for 25 years in a row. Over the past decade, this dividend champion has managed to boost distributions by 8.80% per year. Chevron currently trades at 8.30 times earnings and yields 3.20%. (analysis)

Air Products and Chemicals, Inc. (APD) provides atmospheric gases, process and specialty gases, performance materials, equipment, and services worldwide. The company has raised dividends for 30 years in a row. Over the past decade, this dividend champion has managed to boost distributions by 11.10% per year. Air Products and Chemicals currently trades at 14.30 times earnings and yields 3.30%. (analysis)

Emerson Electric Co. (EMR) operates as a diversified technology company worldwide. The company has raised dividends for 55 years in a row. Over the past decade, this dividend champion has managed to boost distributions by 6.40% per year. Emerson Electric currently trades at 14.50 times earnings and yields 3.30%. (analysis)

Medtronic, Inc. (MDT) manufactures and sells device-based medical therapies worldwide. The company has raised dividends for 35 years in a row. Over the past decade, this dividend champion has managed to boost distributions by 15.80% per year. Medtronic currently trades at 12 times earnings and yields 2.50%. (analysis)

3M Company (MMM) operates as a diversified technology company worldwide. The company has raised dividends for 54 years in a row. Over the past decade, this dividend champion has managed to boost distributions by 6.20% per year. 3M Company currently trades at 14.10 times earnings and yields 2.70%. (analysis)

Walgreen Co. (WAG), together with its subsidiaries, operates a chain of drugstores in the United States. The company has raised dividends for 37 years in a row. Over the past decade, this dividend champion has managed to boost distributions by 18.90% per year. Walgreen currently trades at 14.50 times earnings and yields 3.50%. (analysis)

Full Disclosure: Long AFL, CVX, APD, EMR, MDT, MMM, WAG, JNJ, KO ,ED

Relevant Articles:

- The next bubble in the making

- Don’t chase High Yielding Stocks Blindly

- We are not in a Dividend Bubble

- Dividend Stocks For Long Term Wealth Accumulation

Wednesday, October 31, 2012

Monday, October 29, 2012

A Record Week for Dividend Increases

There were a record 73 dividend increases over the past week. This was the busiest week for dividend increases I have witnessed since starting this site five years ago. I review dividend increases each week in an effort to uncover hidden dividend gems as well as to keep close tabs on the pulse of dividends paid by companies I own or am in the process of researching.

Below, I have highlighted companies that boosted distributions over the past week and have been raising dividends for at least ten consecutive years. I added a brief commentary behind each company of interest. The companies include:

Aflac Incorporated (AFL), through its subsidiary, American Family Life Assurance Company of Columbus, provides supplemental health and life insurance. The company raised its quarterly distributions by 6.10% to 35 cents/share. This marked the 30th consecutive annual dividend increase for this dividend champion. Yield: 2.80% (analysis)

I recently added to my position in Aflac, given the company’s P/E ratio of 8.20. The company has managed to raise dividends by 20.40%/year over the past decade. Most of the fears behind Aflac stem from fears that its portfolio holds a large portion of European debt. Aflac has been decreasing its position in European debt and owns no toxic Greek debt. Another fear could be the Fukushima disaster, which might increase cancer rates in Japan. At the same time the company is growing operations in Japan and US. Check my analysis of the stock.

V.F. Corporation (VFC) designs and manufactures, or sources from independent contractors various apparel and footwear products primarily in the United States and Europe. The company raised its quarterly distributions by 20.80% to 87 cents/share. This marked the 40th consecutive annual dividend increase for this dividend champion. Yield: 2.20%

The company has managed to more than double earnings since 2003.The company has managed to raise dividends by 10.90%/year over the past decade. I analyzed the company in 2011, but just like today the dividend was quite low. I would consider initiating a position in VF Corp on dips below $140.

Magellan Midstream Partners, L.P. (MMP) engages in the transportation, storage, and distribution of petroleum products in the United States. The MLP raised its quarterly distributions to 48.50 cents/share. This marked the 12th consecutive annual dividend increase for this dividend achiever. Yield: 4.40%

Magellan has managed to boost distributions by 15.80%/year over the past decade. I am adding this MLP to my list of companies to analyze in a future post in order to understand if there is any potential for future distributions hikes.

Tompkins Financial Corporation (TMP) operates as a community-based financial services company in New York. The company raised its quarterly distributions by 5.60% to 36 cents/share. This marked the 26th consecutive annual dividend increase for this dividend champion. Yield: 3.70%

The company has managed to boost distributions by 6.40%/year over the past decade. This was driven by an increase in EPS from $2.11 in 2002 to $2.79 in 2011. I like the company’s predictable dividend growth coupled with an above average dividend yield and sustainable dividend payout based on 2012 earnings. I would add the stock to my list for further research.

The following companies that boosted distributions either do not have a yield above 2.50% or are growing distributions at a very slow pace. In order to live off dividends in retirement, investors need stocks that pay decent current yields, which also boost distributions at or above the rate of inflation. That being said, if any of these companies manage to yield more than 2.50% while growing dividends by more than 6% per year, I would consider them for further analysis.

Brown & Brown, Inc. (BRO), a diversified insurance agency, engages in the marketing and sale of insurance products and services in the United States. The company raised its quarterly distributions by 5.90% to 9 cents/share. This marked the 19th consecutive annual dividend increase for this dividend champion. Yield: 1.40%

Met-Pro Corporation (MPR) manufactures and sells product recovery and pollution control equipment for the purification of air and liquids, fluid handling equipment, and filtration and purification products. The company raised its quarterly distributions by 2.10% to 7.25 cents/share. This marked the 12th consecutive annual dividend increase for this dividend achiever. Yield: 3.30%

Middlesex Water Company (MSEX) owns and operates regulated water utility and wastewater systems in New Jersey, Delaware, and Pennsylvania. The company raised its quarterly distributions by 1.40% to 18.75 cents/share. This marked the 40th consecutive annual dividend increase for this dividend achiever. Yield: 4%

UMB Financial Corporation (UMBF), a multi-bank holding company, provides banking and other financial services to commercial, retail, government, and correspondent bank customers. The company raised its quarterly distributions by 4.90% to 21.50 cents/share. This marked the 22nd consecutive annual dividend increase for this dividend achiever. Yield: 1.90%

MSC Industrial Direct Co., Inc. (MSM), together with its subsidiaries, operates as a direct marketer and distributor of metalworking and maintenance, repair, and operations (MRO) products to industrial customers in the United States. The company raised its quarterly distributions by 20% to 30 cents/share. This marked the 10th consecutive annual dividend increase for this dividend achiever. Yield: 1.70%

Prosperity Bancshares, Inc. (PB) operates as the holding company for Prosperity Bank that provides a range of financial products and services to small and medium-sized businesses, and consumers in Texas. The company raised its quarterly distributions by 10.30% to 21.50 cents/share. This marked the 15th consecutive annual dividend increase for this dividend achiever. Yield: 2.10%

Stepan Company (SCL), together with its subsidiaries, engages in the production and sale of specialty and intermediate chemicals to manufacturers in various industries worldwide. The company raised its quarterly distributions by 14.30% to 16 cents/share. This marked the 45th consecutive annual dividend increase for this dividend champion. Yield: 1.20%

Tennant Company (TNC) engages in designing, manufacturing, and marketing cleaning solutions worldwide. The company raised its quarterly distributions by 5.90% to 18 cents/share. This marked the 40th consecutive annual dividend increase for this dividend champion. Yield: 1.90%

Full Disclosure: Long AFL

Relevant Articles:

- Aflac (AFL) Dividend Stock Analysis

- Dividend Champions - The Best List for Dividend Investors

- V.F. Corporation (VFC) Dividend Stock Analysis 2011

- Dividend Achievers Offer Income Growth and Capital Appreciation Potential

Below, I have highlighted companies that boosted distributions over the past week and have been raising dividends for at least ten consecutive years. I added a brief commentary behind each company of interest. The companies include:

Aflac Incorporated (AFL), through its subsidiary, American Family Life Assurance Company of Columbus, provides supplemental health and life insurance. The company raised its quarterly distributions by 6.10% to 35 cents/share. This marked the 30th consecutive annual dividend increase for this dividend champion. Yield: 2.80% (analysis)

I recently added to my position in Aflac, given the company’s P/E ratio of 8.20. The company has managed to raise dividends by 20.40%/year over the past decade. Most of the fears behind Aflac stem from fears that its portfolio holds a large portion of European debt. Aflac has been decreasing its position in European debt and owns no toxic Greek debt. Another fear could be the Fukushima disaster, which might increase cancer rates in Japan. At the same time the company is growing operations in Japan and US. Check my analysis of the stock.

V.F. Corporation (VFC) designs and manufactures, or sources from independent contractors various apparel and footwear products primarily in the United States and Europe. The company raised its quarterly distributions by 20.80% to 87 cents/share. This marked the 40th consecutive annual dividend increase for this dividend champion. Yield: 2.20%

The company has managed to more than double earnings since 2003.The company has managed to raise dividends by 10.90%/year over the past decade. I analyzed the company in 2011, but just like today the dividend was quite low. I would consider initiating a position in VF Corp on dips below $140.

Magellan Midstream Partners, L.P. (MMP) engages in the transportation, storage, and distribution of petroleum products in the United States. The MLP raised its quarterly distributions to 48.50 cents/share. This marked the 12th consecutive annual dividend increase for this dividend achiever. Yield: 4.40%

Magellan has managed to boost distributions by 15.80%/year over the past decade. I am adding this MLP to my list of companies to analyze in a future post in order to understand if there is any potential for future distributions hikes.

Tompkins Financial Corporation (TMP) operates as a community-based financial services company in New York. The company raised its quarterly distributions by 5.60% to 36 cents/share. This marked the 26th consecutive annual dividend increase for this dividend champion. Yield: 3.70%

The company has managed to boost distributions by 6.40%/year over the past decade. This was driven by an increase in EPS from $2.11 in 2002 to $2.79 in 2011. I like the company’s predictable dividend growth coupled with an above average dividend yield and sustainable dividend payout based on 2012 earnings. I would add the stock to my list for further research.

The following companies that boosted distributions either do not have a yield above 2.50% or are growing distributions at a very slow pace. In order to live off dividends in retirement, investors need stocks that pay decent current yields, which also boost distributions at or above the rate of inflation. That being said, if any of these companies manage to yield more than 2.50% while growing dividends by more than 6% per year, I would consider them for further analysis.

Brown & Brown, Inc. (BRO), a diversified insurance agency, engages in the marketing and sale of insurance products and services in the United States. The company raised its quarterly distributions by 5.90% to 9 cents/share. This marked the 19th consecutive annual dividend increase for this dividend champion. Yield: 1.40%

Met-Pro Corporation (MPR) manufactures and sells product recovery and pollution control equipment for the purification of air and liquids, fluid handling equipment, and filtration and purification products. The company raised its quarterly distributions by 2.10% to 7.25 cents/share. This marked the 12th consecutive annual dividend increase for this dividend achiever. Yield: 3.30%

Middlesex Water Company (MSEX) owns and operates regulated water utility and wastewater systems in New Jersey, Delaware, and Pennsylvania. The company raised its quarterly distributions by 1.40% to 18.75 cents/share. This marked the 40th consecutive annual dividend increase for this dividend achiever. Yield: 4%

UMB Financial Corporation (UMBF), a multi-bank holding company, provides banking and other financial services to commercial, retail, government, and correspondent bank customers. The company raised its quarterly distributions by 4.90% to 21.50 cents/share. This marked the 22nd consecutive annual dividend increase for this dividend achiever. Yield: 1.90%

MSC Industrial Direct Co., Inc. (MSM), together with its subsidiaries, operates as a direct marketer and distributor of metalworking and maintenance, repair, and operations (MRO) products to industrial customers in the United States. The company raised its quarterly distributions by 20% to 30 cents/share. This marked the 10th consecutive annual dividend increase for this dividend achiever. Yield: 1.70%

Prosperity Bancshares, Inc. (PB) operates as the holding company for Prosperity Bank that provides a range of financial products and services to small and medium-sized businesses, and consumers in Texas. The company raised its quarterly distributions by 10.30% to 21.50 cents/share. This marked the 15th consecutive annual dividend increase for this dividend achiever. Yield: 2.10%

Stepan Company (SCL), together with its subsidiaries, engages in the production and sale of specialty and intermediate chemicals to manufacturers in various industries worldwide. The company raised its quarterly distributions by 14.30% to 16 cents/share. This marked the 45th consecutive annual dividend increase for this dividend champion. Yield: 1.20%

Tennant Company (TNC) engages in designing, manufacturing, and marketing cleaning solutions worldwide. The company raised its quarterly distributions by 5.90% to 18 cents/share. This marked the 40th consecutive annual dividend increase for this dividend champion. Yield: 1.90%

Full Disclosure: Long AFL

Relevant Articles:

- Aflac (AFL) Dividend Stock Analysis

- Dividend Champions - The Best List for Dividend Investors

- V.F. Corporation (VFC) Dividend Stock Analysis 2011

- Dividend Achievers Offer Income Growth and Capital Appreciation Potential

Friday, October 26, 2012

Harris Corporation (HRS) Dividend Stock Analysis

Harris Corporation (HRS), together with its subsidiaries, operates as an international communications and information technology company that serves government and commercial markets worldwide. The company operates in three segments; RF Communications, Integrated Network Solutions, and Government Communications Systems. The company is a member of the dividend aristocrats’ index, has paid dividends since 1941 and increased them for 11 years in a row.

The company’s last dividend increase was in August 2012 when the Board of Directors approved a 12.10% increase to 37 cents/share. This was the second dividend increase in under one year. The company’s largest competitors include Boeing (BA), Raytheon (RTN) and General Dynamics (GD).

Over the past decade this dividend growth stock has delivered an annualized total return of 11.70% to its shareholders.

The company has managed to an impressive increase in annual EPS growth since 2003. Earnings per share have risen from $0.45/share in 2003 to $4.80/share in 2012. Analysts expect Harris Corporation to earn $5.16 per share in 2013 and $5.28 per share in 2014.

The company has reduced its share count from 133 million shares in 2003 to 114 million in 2012. Most of the buyback activity has happened since 2011. The company is also planning to divest its Broadcasting business segment, and utilize the cash proceeds to further repurchase shares.

Growth in government communications segment as well as recent acquisitions in integrated network solutions are expected to drive revenues for the company. Continued investment in R&D could also result in wider operating margins, which could positively affect profitability. Many Federal and local governments are expected to increase the capabilities of their communications networks, which could bode well for Harris Corporation.

The return on equity has increased from 5% in 2003 to 25% in 2012. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

The annual dividend payment has increased by 26.60% per year over the past decade, which is higher than the growth in EPS.

A 26% growth in distributions translates into the dividend payment doubling almost every three and a half years. If we look at historical data, going as far back as 1999 we see that Harris Corporation has indeed managed to double its dividend every three years on average.

The dividend payout ratio declined from 35% in 2003 to 12.80% in 2007, before beginning a new uptrend all the way to 25% in 2012. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently, Harris Corporation is attractively valued at 9.80 times earnings, has an adequately covered dividend and yields 3.10%. I would consider initiating a position in the stock subject to availability of funds.

Full Disclosure: None

Relevant Articles:

- Three High Dividend Stocks Raising Distributions

- Dividend Achievers Additions for 2012

- Dividend Stocks Offering Positive Feedback to Investors

- How to retire with dividend stocks

The company’s last dividend increase was in August 2012 when the Board of Directors approved a 12.10% increase to 37 cents/share. This was the second dividend increase in under one year. The company’s largest competitors include Boeing (BA), Raytheon (RTN) and General Dynamics (GD).

Over the past decade this dividend growth stock has delivered an annualized total return of 11.70% to its shareholders.

The company has managed to an impressive increase in annual EPS growth since 2003. Earnings per share have risen from $0.45/share in 2003 to $4.80/share in 2012. Analysts expect Harris Corporation to earn $5.16 per share in 2013 and $5.28 per share in 2014.

The company has reduced its share count from 133 million shares in 2003 to 114 million in 2012. Most of the buyback activity has happened since 2011. The company is also planning to divest its Broadcasting business segment, and utilize the cash proceeds to further repurchase shares.

Growth in government communications segment as well as recent acquisitions in integrated network solutions are expected to drive revenues for the company. Continued investment in R&D could also result in wider operating margins, which could positively affect profitability. Many Federal and local governments are expected to increase the capabilities of their communications networks, which could bode well for Harris Corporation.

The return on equity has increased from 5% in 2003 to 25% in 2012. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

The annual dividend payment has increased by 26.60% per year over the past decade, which is higher than the growth in EPS.

A 26% growth in distributions translates into the dividend payment doubling almost every three and a half years. If we look at historical data, going as far back as 1999 we see that Harris Corporation has indeed managed to double its dividend every three years on average.

The dividend payout ratio declined from 35% in 2003 to 12.80% in 2007, before beginning a new uptrend all the way to 25% in 2012. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently, Harris Corporation is attractively valued at 9.80 times earnings, has an adequately covered dividend and yields 3.10%. I would consider initiating a position in the stock subject to availability of funds.

Full Disclosure: None

Relevant Articles:

- Three High Dividend Stocks Raising Distributions

- Dividend Achievers Additions for 2012

- Dividend Stocks Offering Positive Feedback to Investors

- How to retire with dividend stocks

Wednesday, October 24, 2012

Dividends versus Homemade Dividends

Some investors question whether dividends offer any real value to investors. One of their main arguments against dividends is that on the ex-dividend date, the stock price decreases exactly by the amount of the dividend.

The argument goes on further to mention that it should not matter to investors whether they buy a stock yielding 4%, or sell 4% of their portfolio. I am using four percent after the famous four percent rule for retirement. Using both scenarios, the investor will have the same amount of cash. Selling off a portion of one’s portfolio in order to generate cash is regarded as “homemade dividend”. There are several issues with this flawed reasoning.

First, when someone sells a portion of their portfolio, they end up with less shares. If the stock price stays flat, the investor is essentially depleting their asset base. The only way that this strategy would work without depleting your nest egg will be if the share price keeps increasing. Sometimes share prices fall or stay flat for extended periods of time, which could spell trouble for these investors. For example, retirees who relied on the traditional 4% withdrawal rule since 2000 and invested in S&P 500 index funds would have less than 7 years worth of expenses covered. If you are a male, and retired at the age of 62 in 2000, you have approximately 12 more years to live according to the Social Security Administration Longevity Calculator. To summarize, selling a portion of your portfolio to generate cash for living expenses is the same type of advice that people followed when refinancing their homes in order to obtain more cash from their home equity. On the other hand, investors who receive a dividend have cash in hand and the same number of shares. The only difference is that the company has less cash on hand, while the present value of the earnings stream is the same in both situations.

Second, just because a stock price supposedly decreases by the amount of the dividend on the ex-dividend date, doesn’t mean that dividends and homemade dividends are the same thing. Dividends come from earnings that the company paying them has generated. As a result, the dividend is directly connected to the company’s fundamentals. The stock price on the other hand is something completely separate from the underlying business in the short run. In the long run, a stock price is determined by profitability and expectations of profitability. A company which sells for $10/share, but distributed a $10 special cash dividend will not trade at $0 if it is still in business and earning money.

If we make an analogy with bonds, one would note that the prices for both bonds and dividend stocks are decreased by the distribution amount on the ex-dividend date. With bonds however, interest is accrued daily and when you sell the security before the distribution date, you still get a prorated portion of the distribution. For example, let us assume that an investor purchases a 6% bond that pays every 6 months. The bond investor would then receive $30 on a $1000 bond on June 30 and $30 on December 31. By Mar 31, the bond has accumulated an accrued interest amount of 1.50%. If the investor manages to sell the bond at some random price, say 100%, the investor would actually receive the proceeds from the price and the accumulated interest for a total gain of 1.50%. It is interesting to note that dividend haters always focus on the ex-dividend date when discussing their opinions that dividends and homemade dividends are the same thing. In fact, dividend stocks probably also accrue the dividend amount over time. As a result, investors do not really “lose” anything when ex-dividend date comes. In fact, this is mostly a cosmetic change, since stock prices are not directly tied to fundamentals but to other factors. Because stock prices fluctuate all the time, what truly affects stock prices is earnings, economic expectations, inflation interest rates, investor sentiment, the fact that stock prices are trading “ex-dividend” doesn’t really show on stock prices, unless a large special dividend is being paid out. As a result, stock dividends are already “calculated” by the marketplace and added to the stock’s valuation.

For my retirement plan, I am exclusively relying on dividend growth stocks. I might receive Social Security one day, and I do have a 401(k) plan which I have enrolled simply for my employer match. I invest any funds I save and any dividends I receive into more income securities. I recently purchased the following stocks over the past month:

Chevron Corporation (CVX), through its subsidiaries, engages in petroleum, chemicals, mining, power generation, and energy operations worldwide. The company has managed to boost distributions for 25 years in a row. Over the past decade, Chevron has raised dividends by 8.80%/year on average. Yield: 3.20% (analysis)

Aflac Incorporated (AFL), through its subsidiary, American Family Life Assurance Company of Columbus, provides supplemental health and life insurance. The company has managed to boost distributions for 29 years in a row. Over the past decade, Aflac has raised dividends by 20.40%/year on average. Yield: 2.70% (analysis)

Unilever PLC (UL) operates as a fast-moving consumer goods company in Asia, Africa, Europe, and the Americas. The company has managed to boost distributions for 12 years in a row. Over the past decade, Unilever has raised dividends by 9.90%/year on average. Yield: 3.20% (analysis)

Air Products and Chemicals, Inc. (APD) provides atmospheric gases, process and specialty gases, performance materials, equipment, and services worldwide. The company has managed to boost distributions for 30 years in a row. Over the past decade, Air Products and Chemicals has raised dividends by 11.10%/year on average. Yield: 3.10% (analysis)

Abbott Laboratories (ABT) engages in the discovery, development, manufacture, and sale of health care products worldwide. The company has managed to boost distributions for 40 years in a row. Over the past decade, Abbott Laboratories has raised dividends by 8.70%/year on average. Yield: 3.20% (analysis)

Update: Dave Van Knapp wrote an excellent article on Why Selling A Few Shares Is Not The Same As Getting A Dividend

Check the comments on Seeking Alpha for this article as well: Dividends Versus Homemade Dividends

Full Disclosure: Long CVX, AFL, UL, APD, ABT

Relevant Articles:

- Why I am a dividend growth investor?

- Why should companies pay out dividends?

- How to avoid being a dividend loser

- How to be a Dividend Winner

The argument goes on further to mention that it should not matter to investors whether they buy a stock yielding 4%, or sell 4% of their portfolio. I am using four percent after the famous four percent rule for retirement. Using both scenarios, the investor will have the same amount of cash. Selling off a portion of one’s portfolio in order to generate cash is regarded as “homemade dividend”. There are several issues with this flawed reasoning.

First, when someone sells a portion of their portfolio, they end up with less shares. If the stock price stays flat, the investor is essentially depleting their asset base. The only way that this strategy would work without depleting your nest egg will be if the share price keeps increasing. Sometimes share prices fall or stay flat for extended periods of time, which could spell trouble for these investors. For example, retirees who relied on the traditional 4% withdrawal rule since 2000 and invested in S&P 500 index funds would have less than 7 years worth of expenses covered. If you are a male, and retired at the age of 62 in 2000, you have approximately 12 more years to live according to the Social Security Administration Longevity Calculator. To summarize, selling a portion of your portfolio to generate cash for living expenses is the same type of advice that people followed when refinancing their homes in order to obtain more cash from their home equity. On the other hand, investors who receive a dividend have cash in hand and the same number of shares. The only difference is that the company has less cash on hand, while the present value of the earnings stream is the same in both situations.

Second, just because a stock price supposedly decreases by the amount of the dividend on the ex-dividend date, doesn’t mean that dividends and homemade dividends are the same thing. Dividends come from earnings that the company paying them has generated. As a result, the dividend is directly connected to the company’s fundamentals. The stock price on the other hand is something completely separate from the underlying business in the short run. In the long run, a stock price is determined by profitability and expectations of profitability. A company which sells for $10/share, but distributed a $10 special cash dividend will not trade at $0 if it is still in business and earning money.

If we make an analogy with bonds, one would note that the prices for both bonds and dividend stocks are decreased by the distribution amount on the ex-dividend date. With bonds however, interest is accrued daily and when you sell the security before the distribution date, you still get a prorated portion of the distribution. For example, let us assume that an investor purchases a 6% bond that pays every 6 months. The bond investor would then receive $30 on a $1000 bond on June 30 and $30 on December 31. By Mar 31, the bond has accumulated an accrued interest amount of 1.50%. If the investor manages to sell the bond at some random price, say 100%, the investor would actually receive the proceeds from the price and the accumulated interest for a total gain of 1.50%. It is interesting to note that dividend haters always focus on the ex-dividend date when discussing their opinions that dividends and homemade dividends are the same thing. In fact, dividend stocks probably also accrue the dividend amount over time. As a result, investors do not really “lose” anything when ex-dividend date comes. In fact, this is mostly a cosmetic change, since stock prices are not directly tied to fundamentals but to other factors. Because stock prices fluctuate all the time, what truly affects stock prices is earnings, economic expectations, inflation interest rates, investor sentiment, the fact that stock prices are trading “ex-dividend” doesn’t really show on stock prices, unless a large special dividend is being paid out. As a result, stock dividends are already “calculated” by the marketplace and added to the stock’s valuation.

For my retirement plan, I am exclusively relying on dividend growth stocks. I might receive Social Security one day, and I do have a 401(k) plan which I have enrolled simply for my employer match. I invest any funds I save and any dividends I receive into more income securities. I recently purchased the following stocks over the past month:

Chevron Corporation (CVX), through its subsidiaries, engages in petroleum, chemicals, mining, power generation, and energy operations worldwide. The company has managed to boost distributions for 25 years in a row. Over the past decade, Chevron has raised dividends by 8.80%/year on average. Yield: 3.20% (analysis)

Aflac Incorporated (AFL), through its subsidiary, American Family Life Assurance Company of Columbus, provides supplemental health and life insurance. The company has managed to boost distributions for 29 years in a row. Over the past decade, Aflac has raised dividends by 20.40%/year on average. Yield: 2.70% (analysis)

Unilever PLC (UL) operates as a fast-moving consumer goods company in Asia, Africa, Europe, and the Americas. The company has managed to boost distributions for 12 years in a row. Over the past decade, Unilever has raised dividends by 9.90%/year on average. Yield: 3.20% (analysis)

Air Products and Chemicals, Inc. (APD) provides atmospheric gases, process and specialty gases, performance materials, equipment, and services worldwide. The company has managed to boost distributions for 30 years in a row. Over the past decade, Air Products and Chemicals has raised dividends by 11.10%/year on average. Yield: 3.10% (analysis)

Abbott Laboratories (ABT) engages in the discovery, development, manufacture, and sale of health care products worldwide. The company has managed to boost distributions for 40 years in a row. Over the past decade, Abbott Laboratories has raised dividends by 8.70%/year on average. Yield: 3.20% (analysis)

Update: Dave Van Knapp wrote an excellent article on Why Selling A Few Shares Is Not The Same As Getting A Dividend

Check the comments on Seeking Alpha for this article as well: Dividends Versus Homemade Dividends

Full Disclosure: Long CVX, AFL, UL, APD, ABT

Relevant Articles:

- Why I am a dividend growth investor?

- Why should companies pay out dividends?

- How to avoid being a dividend loser

- How to be a Dividend Winner

Monday, October 22, 2012

Eight Income Stocks Bringing Joy to Their Investors

John D Rockefeller, the founder of Standard Oil is famous for saying that the only thing bringing him joy in life was the sound of his dividends being deposited in his account. The heirs of the Standard Oil tycoon have been living off these oil dividends for several generations now. Dividend payments give these investors the opportunity to generate income without having to sell shares, and are typically a less volatile source of total returns than capital gains alone. In this article, I have highlighted several consistent dividend increasers, and provided a brief comment on each stock.

The shareholders of the following consistent income payers are not only getting paid to hold their income stocks, but also received a dividend hike over the past week:

Kinder Morgan Energy Partners, L.P. (KMP) operates as a pipeline transportation and energy storage company in North America. The partnership increased quarterly distributions to $1.26/unit. This dividend achiever has consistently boosted distributions for 16 years in a row. Yield: 5.90%

Kinder Morgan does have the distributable cash flows from its vast portfolio of fee generating assets to pay for its generous partner distributions. In addition, the partnership is raising distributable cash flow per unit by investing in new assets and making strategic acquisitions. Check my recent analysis of Kinder Morgan Partnership.

Eaton Vance Corp. (EV), through its subsidiaries, engages in the creation, marketing, and management of investment funds in the United States. The company raised its quarterly distributions by 5.30% to 20 cents/share. This marked the 32nd consecutive annual dividend increase for this dividend champion. Yield: 2.80%

The latest dividend increase is much lower than the ten year average annual dividend hike of 19.20%. Overall I am bullish on asset managers, and find the sector to be the best bet on the long term secular trends such as increasing need for investment in products such as mutual funds by Baby Boomers. The company is attractively valued at 17.30 times earnings. I plan on adding to my position in the stock subject to availability of funds. Check my analysis of the stock.

Aqua America, Inc. (WTR), through its subsidiaries, operates regulated utilities that provide water or wastewater services in the United States. The company raised its quarterly distributions by 6.10% to 17.50 cents/share. This marked the 22nd consecutive annual dividend increase for this dividend achiever. Yield: 2.80%

Over the past decade, Aqua America has managed to boost dividends at an annual rate of 7.60%. In addition, the company has managed to double earnings per share since 2002. The company however is overvalued at 23 times earnings right now. I would consider researching the company in more detail in the future, and potentially initiating a position on dips below $22/share.

Westwood Holdings Group, Inc. (WHG) manages investment assets and provides services for its clients. The company raised its quarterly distributions by 8.10% to 40 cents/share. This marked the 12th consecutive annual dividend increase for this dividend achiever. Yield: 4.20%

Asset managers are destined to have a bright future as a group, as millions of investors in the US are saving for an uncertain future with limited or no pensions from governments or employers. I like the history of dividend growth for Westwood as well as the increase in earnings over the past decade from 97 cent/share in 2002 to $2.11/share in 2011. The company also tends to distribute special dividends every now and then to shareholders, although the last such distribution has been made in 2010. Unfortunately, the stock is overvalued at 21 times earnings and has a dividend payout ratio of over 80%. I would consider reviewing the stock in more detail if it manages to lower dividend payout ratio to 60% or less.

Omega Healthcare Investors, Inc. (OHI) operates as a real estate investment trust (REIT) in the United States. The REIT raised quarterly distributions to 44 cents/share. Omega Healthcare Investors has boosted distributions for 10 years in a row. Yield: 7.30%

If you dig into the historical distributions in this REIT, one would notice how dividends went from $2.80/share in 1999 to nothing in 2001 and 2002. Omega Healthcare Investors then initiated dividends again in 2003 and has been raising them ever since. I would consider researching this REIT in a future article, in order to uncover what caused it to cut dividends in 2000, and what is the likelihood of this occurring again.

A. Schulman, Inc. (SHLM) supplies plastic compounds and resins for packaging, consumer products, industrial, and automotive applications. The company raised its quarterly distributions by 2.60% to 19.50 cents/share. This marked the sixth consecutive annual dividend increase for this dividend stock. Yield: 3.20%

The company has delivered a very anemic 1.60% in annual dividend hikes over the past decade. In addition, its earnings are a little too volatile to support consistent dividend increases in the future. Despite the high yields at 3.20% and attractive valuation at 15.70 times earnings, the low earnings and dividend growth is a red flag. The high volatility in earnings over the past decade, and the short history of dividend increases makes this stock a hold. Since 1986 the company has never cut distributions, but it tends to raise them for a few years, and then freeze them, until it resumes a slow action of dividend hikes.

Cass Information Systems, Inc. (CASS) provides payment and information processing services to manufacturing, distribution, and retail enterprises in the United States. The company raised its quarterly distributions by 16.50% to 18 cents/share. This marked the eleventh consecutive annual dividend increase for this dividend achiever. Yield: 1.70%

The ten year average annual dividend growth rate for Cass Information Systems is 9.10%. I like the the fact that the company has managed to triple earnings per share over the past decade to $2.23/share in 2011. Unfortunately, the current yield of 1.70% is a little too low for me. Nevertheless, the company exhibits the characteristics that merit future analysis on this site.

Cintas Corporation (CTAS) provides corporate identity uniforms and related business services for approximately 900,000 businesses in North America, Latin America, Europe, and Asia. The company raised its annual distribution by 18.50% to 64 cents/share. This marked the 30th consecutive annual dividend increase for this dividend champion. Yield: 1.50%

Cintas has managed to boost dividends by 9.10%/year over the past decade. In addition, earnings per share have increased from $1.46 in 2003 to $2.37 in 2011. Analysts expect Cintas to grow EPS to $2.55 in 2012 and $2.81 by 2014. The company is also attractively valued at 17.80 times earnings, but unfortunately yields only 1.50%. With my entry criteria of 2.50%, the stock needs to drop significantly from current levels before it reaches buy territory. Nevertheless, I would consider adding the stock to my list for further analysis.

Full Disclosure: Long KMR, KMI and EV

Relevant Articles:

- Kinder Morgan Partners (KMP) for High Yield and Solid Distributions Growth

- Eaton Vance (EV) Dividend Stock Analysis 2011

- Dividend Macro trends: The Baby Boomer Retirement Investment

- Master Limited Partnerships (MLPs) – an island of opportunity for dividend investors

The shareholders of the following consistent income payers are not only getting paid to hold their income stocks, but also received a dividend hike over the past week:

Kinder Morgan Energy Partners, L.P. (KMP) operates as a pipeline transportation and energy storage company in North America. The partnership increased quarterly distributions to $1.26/unit. This dividend achiever has consistently boosted distributions for 16 years in a row. Yield: 5.90%

Kinder Morgan does have the distributable cash flows from its vast portfolio of fee generating assets to pay for its generous partner distributions. In addition, the partnership is raising distributable cash flow per unit by investing in new assets and making strategic acquisitions. Check my recent analysis of Kinder Morgan Partnership.

Eaton Vance Corp. (EV), through its subsidiaries, engages in the creation, marketing, and management of investment funds in the United States. The company raised its quarterly distributions by 5.30% to 20 cents/share. This marked the 32nd consecutive annual dividend increase for this dividend champion. Yield: 2.80%

The latest dividend increase is much lower than the ten year average annual dividend hike of 19.20%. Overall I am bullish on asset managers, and find the sector to be the best bet on the long term secular trends such as increasing need for investment in products such as mutual funds by Baby Boomers. The company is attractively valued at 17.30 times earnings. I plan on adding to my position in the stock subject to availability of funds. Check my analysis of the stock.

Aqua America, Inc. (WTR), through its subsidiaries, operates regulated utilities that provide water or wastewater services in the United States. The company raised its quarterly distributions by 6.10% to 17.50 cents/share. This marked the 22nd consecutive annual dividend increase for this dividend achiever. Yield: 2.80%

Over the past decade, Aqua America has managed to boost dividends at an annual rate of 7.60%. In addition, the company has managed to double earnings per share since 2002. The company however is overvalued at 23 times earnings right now. I would consider researching the company in more detail in the future, and potentially initiating a position on dips below $22/share.

Westwood Holdings Group, Inc. (WHG) manages investment assets and provides services for its clients. The company raised its quarterly distributions by 8.10% to 40 cents/share. This marked the 12th consecutive annual dividend increase for this dividend achiever. Yield: 4.20%

Asset managers are destined to have a bright future as a group, as millions of investors in the US are saving for an uncertain future with limited or no pensions from governments or employers. I like the history of dividend growth for Westwood as well as the increase in earnings over the past decade from 97 cent/share in 2002 to $2.11/share in 2011. The company also tends to distribute special dividends every now and then to shareholders, although the last such distribution has been made in 2010. Unfortunately, the stock is overvalued at 21 times earnings and has a dividend payout ratio of over 80%. I would consider reviewing the stock in more detail if it manages to lower dividend payout ratio to 60% or less.

Omega Healthcare Investors, Inc. (OHI) operates as a real estate investment trust (REIT) in the United States. The REIT raised quarterly distributions to 44 cents/share. Omega Healthcare Investors has boosted distributions for 10 years in a row. Yield: 7.30%

If you dig into the historical distributions in this REIT, one would notice how dividends went from $2.80/share in 1999 to nothing in 2001 and 2002. Omega Healthcare Investors then initiated dividends again in 2003 and has been raising them ever since. I would consider researching this REIT in a future article, in order to uncover what caused it to cut dividends in 2000, and what is the likelihood of this occurring again.

A. Schulman, Inc. (SHLM) supplies plastic compounds and resins for packaging, consumer products, industrial, and automotive applications. The company raised its quarterly distributions by 2.60% to 19.50 cents/share. This marked the sixth consecutive annual dividend increase for this dividend stock. Yield: 3.20%

The company has delivered a very anemic 1.60% in annual dividend hikes over the past decade. In addition, its earnings are a little too volatile to support consistent dividend increases in the future. Despite the high yields at 3.20% and attractive valuation at 15.70 times earnings, the low earnings and dividend growth is a red flag. The high volatility in earnings over the past decade, and the short history of dividend increases makes this stock a hold. Since 1986 the company has never cut distributions, but it tends to raise them for a few years, and then freeze them, until it resumes a slow action of dividend hikes.

Cass Information Systems, Inc. (CASS) provides payment and information processing services to manufacturing, distribution, and retail enterprises in the United States. The company raised its quarterly distributions by 16.50% to 18 cents/share. This marked the eleventh consecutive annual dividend increase for this dividend achiever. Yield: 1.70%

The ten year average annual dividend growth rate for Cass Information Systems is 9.10%. I like the the fact that the company has managed to triple earnings per share over the past decade to $2.23/share in 2011. Unfortunately, the current yield of 1.70% is a little too low for me. Nevertheless, the company exhibits the characteristics that merit future analysis on this site.

Cintas Corporation (CTAS) provides corporate identity uniforms and related business services for approximately 900,000 businesses in North America, Latin America, Europe, and Asia. The company raised its annual distribution by 18.50% to 64 cents/share. This marked the 30th consecutive annual dividend increase for this dividend champion. Yield: 1.50%

Cintas has managed to boost dividends by 9.10%/year over the past decade. In addition, earnings per share have increased from $1.46 in 2003 to $2.37 in 2011. Analysts expect Cintas to grow EPS to $2.55 in 2012 and $2.81 by 2014. The company is also attractively valued at 17.80 times earnings, but unfortunately yields only 1.50%. With my entry criteria of 2.50%, the stock needs to drop significantly from current levels before it reaches buy territory. Nevertheless, I would consider adding the stock to my list for further analysis.

Full Disclosure: Long KMR, KMI and EV

Relevant Articles:

- Kinder Morgan Partners (KMP) for High Yield and Solid Distributions Growth

- Eaton Vance (EV) Dividend Stock Analysis 2011

- Dividend Macro trends: The Baby Boomer Retirement Investment

- Master Limited Partnerships (MLPs) – an island of opportunity for dividend investors

Friday, October 19, 2012

Kinder Morgan Partners (KMP) for High Yield and Solid Distributions Growth

Kinder Morgan Energy Partners, L.P. (KMP) operates as a pipeline transportation and energy storage company in North America. The partnership is a member of the dividend achievers index, as it has managed to boost quarterly distributions for 16 consecutive years. Over the past decade, Kinder Morgan has managed to boost distributions by 8.20%/year. The partnership operates over 75,000 miles of pipelines as well as 180 terminals.

Its main business activity involves transporting commodities such as oil and natural gas for third parties such as oil and gas companies for a fee. In essence, Kinder Morgan operates a toll-based business, which generates stable fee revenues, without having exposure to fluctuating commodity prices. The volumes of oil and gas transported in the US are very stable and move by only a few percentage points per year. In addition, as the US is experiencing a boom in shale-gas production, there is a greater need for transporting carbons in the country. Companies like Kinder Morgan are in a great position to capitalize on this opportunity, with their pipelines in Marcellus Shale, Eagle Ford, Haynesville and Barnett Shale.

The partnership is operated by Kinder Morgan Inc (KMI), which is the General Partner. The general partner has an incentive distribution rights to 50% of distributable cash flows over certain amounts as well as 11% of the partnership. As a result, future distributions growth might be limited in the limited partnership level, but much higher at the general partner level. In a previous article I mentioned that there are three ways to invest in Kinder Morgan through general partner, limited partner and LLC interests.

Kinder Morgan’s CEO, Richard Kinder, owns 24% of the general partner interests in the partnership and received an annual salary of $1/year. As a result, since most of his net worth is invested in the partnership, he has the incentive to deliver solid results to unit holders in terms of distributions and total returns. It is rare in corporate America today to see management and shareholders goals align as closely as they do in Kinder Morgan. The other major company that comes to mind, where top management has a large stake includes Warren Buffett’s Berkshire Hathaway (BRK.B).

As a master limited partnership, Kinder Morgan (KMP) is a pass-through entity. This means that it does not pay taxes at the corporate level. Instead, each unitholder pays their portion of Kinder Morgan’s income, net of any deductions. Each year, unitholders receive a K-1 form, which describes their share of income, and how to report it on their tax returns. In general, for the first ten years or so, new unitholders generally do not pay taxes on their distributions, as they are classified as “return of capital” for tax purposes. While this creates a slightly more challenging tax return than the typical dividend paying stock, any serious do-it-yourself investor or investor with an average CPA should be able to handle this aspect. Taxation also makes investing in Kinder Morgan Partners slightly more challenging in deferred retirement accounts such as ROTH IRA’s. Luckily, the option to acquire i-shares of Kinder Morgan Management (KMR) exists, which pay distributions in the form of stock. As a result, unitholders do not receive any cash, and their distributions are viewed in the eyes of the IRS similar to stock splits. This means that unitholders of Kinder Morgan Partners, who invest in I-Shares such as KMR do not have to file any information with tax authorities regarding the shares they received as distributions from KMR. The only item that has to be reported would be the taxable event of a sale. Currently, KMR trades at a discount to KMP, which is why a lot of investors have chosen it over the partnership units.

This being said, Kinder Morgan does have the distributable cash flows from its vast portfolio of fee generating assets to pay for its generous partner distributions. For the first six months of 2012, Kinder Morgan had Distributable Cash Flow of $2.44 unit, while it paid out $2.36/unit. In 2011 DCF/unit was $4.68/unit and the partnership distributed $4.61/unit for the year.

Future distributions growth could come out of the ten billion in capex that the partnership plans to invest over the next five years. Projects in the pipeline include $4 billion for Transmountain Pipeline expansion, as well as expansions in company’s Natural Gas and Products Pipelines expansions. As General Partner plans on becoming a pure play GP by 2014, there will be expected drop-downs of assets to Kinder Morgan Partners, which would fuel future distributions growth as well. The Parkway Pipeline is another major project in South-East US, which is expected to come on-line in 2013, and be accretive to distributable cash flow per unit. Another driver of growth could include tariff increases as well as organic growth in oil and gas delivered. A third driver of growth could include strategic acquisitions. The acquisition of El Paso in 2011 will lead to Kinder Morgan Partners acquiring several projects. This in turn has increased the expected growth in distributions per unit from 5% to 7% in the foreseeable future.

One of the risks for the partnership includes interest rate risk. For every one percent move in interest rates, interest expense fluctuates by $55 million. If interest rates start to increase, that could affect distributable cash flow per unit, as new projects would be more expensive to build.

Full Disclosure: Long KMR and KMI

Relevant Articles:

- Master Limited Partnerships (MLPs) – an island of opportunity for dividend investors

- General vs Limited Partners in MLP's

- MLPs for tax-deferred accounts

- Kinder Morgan Partners – One Company three ways to invest in it

Its main business activity involves transporting commodities such as oil and natural gas for third parties such as oil and gas companies for a fee. In essence, Kinder Morgan operates a toll-based business, which generates stable fee revenues, without having exposure to fluctuating commodity prices. The volumes of oil and gas transported in the US are very stable and move by only a few percentage points per year. In addition, as the US is experiencing a boom in shale-gas production, there is a greater need for transporting carbons in the country. Companies like Kinder Morgan are in a great position to capitalize on this opportunity, with their pipelines in Marcellus Shale, Eagle Ford, Haynesville and Barnett Shale.

The partnership is operated by Kinder Morgan Inc (KMI), which is the General Partner. The general partner has an incentive distribution rights to 50% of distributable cash flows over certain amounts as well as 11% of the partnership. As a result, future distributions growth might be limited in the limited partnership level, but much higher at the general partner level. In a previous article I mentioned that there are three ways to invest in Kinder Morgan through general partner, limited partner and LLC interests.

Kinder Morgan’s CEO, Richard Kinder, owns 24% of the general partner interests in the partnership and received an annual salary of $1/year. As a result, since most of his net worth is invested in the partnership, he has the incentive to deliver solid results to unit holders in terms of distributions and total returns. It is rare in corporate America today to see management and shareholders goals align as closely as they do in Kinder Morgan. The other major company that comes to mind, where top management has a large stake includes Warren Buffett’s Berkshire Hathaway (BRK.B).

As a master limited partnership, Kinder Morgan (KMP) is a pass-through entity. This means that it does not pay taxes at the corporate level. Instead, each unitholder pays their portion of Kinder Morgan’s income, net of any deductions. Each year, unitholders receive a K-1 form, which describes their share of income, and how to report it on their tax returns. In general, for the first ten years or so, new unitholders generally do not pay taxes on their distributions, as they are classified as “return of capital” for tax purposes. While this creates a slightly more challenging tax return than the typical dividend paying stock, any serious do-it-yourself investor or investor with an average CPA should be able to handle this aspect. Taxation also makes investing in Kinder Morgan Partners slightly more challenging in deferred retirement accounts such as ROTH IRA’s. Luckily, the option to acquire i-shares of Kinder Morgan Management (KMR) exists, which pay distributions in the form of stock. As a result, unitholders do not receive any cash, and their distributions are viewed in the eyes of the IRS similar to stock splits. This means that unitholders of Kinder Morgan Partners, who invest in I-Shares such as KMR do not have to file any information with tax authorities regarding the shares they received as distributions from KMR. The only item that has to be reported would be the taxable event of a sale. Currently, KMR trades at a discount to KMP, which is why a lot of investors have chosen it over the partnership units.

This being said, Kinder Morgan does have the distributable cash flows from its vast portfolio of fee generating assets to pay for its generous partner distributions. For the first six months of 2012, Kinder Morgan had Distributable Cash Flow of $2.44 unit, while it paid out $2.36/unit. In 2011 DCF/unit was $4.68/unit and the partnership distributed $4.61/unit for the year.

Future distributions growth could come out of the ten billion in capex that the partnership plans to invest over the next five years. Projects in the pipeline include $4 billion for Transmountain Pipeline expansion, as well as expansions in company’s Natural Gas and Products Pipelines expansions. As General Partner plans on becoming a pure play GP by 2014, there will be expected drop-downs of assets to Kinder Morgan Partners, which would fuel future distributions growth as well. The Parkway Pipeline is another major project in South-East US, which is expected to come on-line in 2013, and be accretive to distributable cash flow per unit. Another driver of growth could include tariff increases as well as organic growth in oil and gas delivered. A third driver of growth could include strategic acquisitions. The acquisition of El Paso in 2011 will lead to Kinder Morgan Partners acquiring several projects. This in turn has increased the expected growth in distributions per unit from 5% to 7% in the foreseeable future.

One of the risks for the partnership includes interest rate risk. For every one percent move in interest rates, interest expense fluctuates by $55 million. If interest rates start to increase, that could affect distributable cash flow per unit, as new projects would be more expensive to build.

Full Disclosure: Long KMR and KMI

Relevant Articles:

- Master Limited Partnerships (MLPs) – an island of opportunity for dividend investors

- General vs Limited Partners in MLP's

- MLPs for tax-deferred accounts

- Kinder Morgan Partners – One Company three ways to invest in it

Wednesday, October 17, 2012

How to avoid being a dividend loser

Dividend losers focus on excuses that prevent them from achieving their goals of financial freedom. Dividend Winners on the other hand, focus on creating specific goals, and the steps to make them a reality.

The first excuse that dividend losers use relates to the fact that since dividends get taxed at 15% per year, this somehow makes dividend stocks an inferior investment. Dividend losers use companies like Berkshire Hathaway (BRK.B) to prove their point. They do like that fact that it has managed to reinvest dividends from its various subsidiaries into more businesses. They hate to have to research a company, formulate a strategy and execute that strategy however. Reinvesting the dividends from their income portfolio seems like too much work for dividend losers. This makes dividend investing a losing proposition to dividend losers. Unfortunately, there is only one Berkshire Hathaway, while there are over 100 dividend champions – companies which have raised dividends for more than 25 years in a row. While dividend losers are looking for the next Berkshire Hathaway, dividend winners are creating their own Berkshire Hathaway’s with the generous dividends from their portfolios.

Besides the reason behind taxation of dividends, another reason why investors fail to make good investing decisions is because certain pass-through entities generate slightly more complicated tax returns. A prime example of that includes pipeline Master Limited Partnerships such as Kinder Morgan (KMP) as well as Enterprise Product Partners (EPD). Investors should focus on identifying the best opportunities that would deliver the best results first, and only worry about taxes later on. I have witnessed investors who wanted to sell stocks, but did not, because they waited a little longer in order to qualify for a long-term capital gains treatment. After they qualified, the paper gains had evaporated and turned into losses. Warren Buffett for example made his first $20 million by running a hedge fund which was structured similarly to a master limited partnership of today. Investors who avoided his partnership because they did not want to complicate tax returns missed the opportunity of their lifetimes.

Another excuse that dividend losers utilize is that they do not have enough money to start investing. Investors who fail to save a sufficient nest egg, would not be able to retire. Buying high yielding stocks such as American Capital Agency (AGNC) or Hatteras Financial (HTS) is not going to solve that problem. When the spread between short-term interest rates and the rates on mortgage bonds declines, investors would see dividend cuts across the board, which would likely lead to them searching for a job in order to pay for their expenses.

To summarize, in order to avoid being dividend losers, and live off their nest eggs, investors should be able to focus on the best opportunities in the markets first, and worry about other items like taxes later. By being flexible, and adapting your strategy to fit the external environment, and not simply searching internally for strategic insight, would help in avoiding pricey mistakes that could derail one's retirement.

Full disclosure: Long KMR, KMI and EPD

Relevant Artciles:

- How to be a Dividend Winner

- Dividend Champions - The Best List for Dividend Investors

- Build your own Berkshire with dividend paying stocks

- Master Limited Partnerships (MLPs) – an island of opportunity for dividend investors

The first excuse that dividend losers use relates to the fact that since dividends get taxed at 15% per year, this somehow makes dividend stocks an inferior investment. Dividend losers use companies like Berkshire Hathaway (BRK.B) to prove their point. They do like that fact that it has managed to reinvest dividends from its various subsidiaries into more businesses. They hate to have to research a company, formulate a strategy and execute that strategy however. Reinvesting the dividends from their income portfolio seems like too much work for dividend losers. This makes dividend investing a losing proposition to dividend losers. Unfortunately, there is only one Berkshire Hathaway, while there are over 100 dividend champions – companies which have raised dividends for more than 25 years in a row. While dividend losers are looking for the next Berkshire Hathaway, dividend winners are creating their own Berkshire Hathaway’s with the generous dividends from their portfolios.

Besides the reason behind taxation of dividends, another reason why investors fail to make good investing decisions is because certain pass-through entities generate slightly more complicated tax returns. A prime example of that includes pipeline Master Limited Partnerships such as Kinder Morgan (KMP) as well as Enterprise Product Partners (EPD). Investors should focus on identifying the best opportunities that would deliver the best results first, and only worry about taxes later on. I have witnessed investors who wanted to sell stocks, but did not, because they waited a little longer in order to qualify for a long-term capital gains treatment. After they qualified, the paper gains had evaporated and turned into losses. Warren Buffett for example made his first $20 million by running a hedge fund which was structured similarly to a master limited partnership of today. Investors who avoided his partnership because they did not want to complicate tax returns missed the opportunity of their lifetimes.

Another excuse that dividend losers utilize is that they do not have enough money to start investing. Investors who fail to save a sufficient nest egg, would not be able to retire. Buying high yielding stocks such as American Capital Agency (AGNC) or Hatteras Financial (HTS) is not going to solve that problem. When the spread between short-term interest rates and the rates on mortgage bonds declines, investors would see dividend cuts across the board, which would likely lead to them searching for a job in order to pay for their expenses.

To summarize, in order to avoid being dividend losers, and live off their nest eggs, investors should be able to focus on the best opportunities in the markets first, and worry about other items like taxes later. By being flexible, and adapting your strategy to fit the external environment, and not simply searching internally for strategic insight, would help in avoiding pricey mistakes that could derail one's retirement.

Full disclosure: Long KMR, KMI and EPD

Relevant Artciles:

- How to be a Dividend Winner

- Dividend Champions - The Best List for Dividend Investors

- Build your own Berkshire with dividend paying stocks

- Master Limited Partnerships (MLPs) – an island of opportunity for dividend investors

Monday, October 15, 2012

Six Dividend Winners Boosting Investor's Distributions

In this article, I have highlighted several companies whose Boards of Directors approved increases in distributions over the past week. In order to reduce the list to a more manageable level, I only highlighted companies which have managed to boost dividends for at least five years in a row. I use five years as an initial screen, because it is roughly equal to the average economic cycle. By only including companies which have raised dividends for at least five years in row, I am only including companies which have demonstrated the ability to hike distributions for longer than one economic cycle.

The consistent dividend raisers of the past week include:

Northwest Natural Gas Company (NWN) stores and distributes natural gas primarily in Oregon, Washington, and California. The company raised quarterly distributions by 2.20% to 45.50 cents/share. This dividend king has boosted distributions for 57 years in a row. Yield: 3.60%

This utility has managed to boost earnings from $1.63/share in 2002 to $2.39 in 2011. The ten year dividend growth is 3.50%/year, which is not bad for a utility. In addition, its current payout ratio of 76.50% is not too bad for a utility either. After I sold the majority of my Con Edison (ED) position, I have been on the lookout for utility companies to add to my portfolio. I would consider analyzing the stock in more detail in the coming weeks.

Fastenal Company (FAST), together with its subsidiaries, operates as a wholesaler and retailer of industrial and construction supplies in the United States and internationally. This dividend achiever raised quarterly distributions by 10.50% to 21 cents/share. Fastenal has boosted distributions for 14 years in a row. Yield: 1.80%

I like the fundamentals behind Fastenal, as well as the strong earnings growth over the past decade. In addition, I also like the strong potential for future earnings growth. One drawback behind Fastenal is the high valuation. The stock trades at over 33 times earnings and yields only 1.80%. I would consider initiating a position in the stock on dips to my buy zone between $27 - $30/share.

Targa Resources Partners LP (NGLS) provides midstream natural gas and natural gas liquid (NGL) services in the United States. This master limited partnership raised quarterly distributions to 66.25 cents/unit. Targa Resources Partners has boosted distributions for 6 years in a row. Yield: 6%

The partnership has been able to cover distributions from distributable cash flow at 1.15 times in Q2 2012, 1.5 times in Q1 2012, 1.6 times in Q4 2011 and 1.10 times DCF in Q3 2011. In addition, the partnership has also been able to boost distributable cash flow in order to be able to pay rising distributions over the past six years. I would like to see at least ten years of dividend hikes before I invest in a stock however. As a result I would add the stock on my watch list in order to see how the business evolves over the next few years

Western Gas Partners, LP (WES) owns, operates, acquires, and develops midstream energy assets in east, west, and south Texas; the Rocky Mountains; and the Mid-Continent. The MLP raised quarterly distributions to 50 cents/unit. Western Gas Partners has boosted distributions for 5 years in a row. Yield: 3.80%

Western Gas Partners has one of the lowest yields for Master Limited Partnerships. However, its ratio of distributions paid to the distributable cash flow has been 1.59 in 2011 and 1.64 in 2010, which is very high for the sector. In addition, it is targeting double digit distribution growth over the next year, due to expansion. I would add this MLP to my list for further research.

Healthcare Services Group, Inc. (HCSG), together with its subsidiaries, provides housekeeping, laundry, linen, facility maintenance, and dietary services to nursing homes, retirement complexes, rehabilitation centers, and hospitals in the United States. This dividend achiever raised quarterly distributions to 16.50 cents/share. Healthcare Services Group has boosted distributions for 10 years in a row. Yield: 2.90%

I like the fact that the company has managed to boost distributions every single quarter since initiating a dividend in 2003. However, I think that the company went too far in raising distributions to an unsustainably high amount. I currently find the dividend payout to be extremely high. As a result, I do not find the current payment to be sustainable. As a result, I would not be able to commit funds to initiate a position in the stock.

Senior Housing Properties Trust (SNH), a real estate investment trust (REIT), primarily invests in senior housing properties in the United States. The company raised quarterly distributions by 2.60% to 39 cents/share. Senior Housing Properties Trust has boosted distributions for 8 years in a row. Yield: 7.10%

A common metric for evaluating REITs is Funds From Operations, which includes earnings and other non-cash offsets such as depreciation. For the past four quarters FFO/share is $1.75, while the forward dividend payment at the new rate is $1.56year. This makes for a FFO payout ratio of 89%, which is slightly high for my liking. I typically prefer an FFO payout in the mid 80’s %. This metric has stood around 84% – 86% between 2009 and 2011, which is why I think that the company might not have a lot of room to grow distributions going forward. FFO/share increased from $1.70/share in 2009 to $1.75/share for the past four quarters through Q2 2012.

Full Disclosure: None

Relevant Articles:

- Eleven Dividend Kings, Raising dividends for 50+ years